I saw an article on Henry Cisneros, Clinton's Top Housing Official. He now has some misgivings about the housing market:

http://www.nytimes.com/2008/10/19/business/19cisneros.html?_r=1&em&oref=slogin

I sent the article on to a friend with some comments. He replied with an email "Thanks for sending the article which I missed in my rush thru the day. I always thought he [Cisneros] was a bad guy, starting from the sex scandal and what I read about him....He is partly to blame. And there are zillions of others....In the housing disaster, more to blame nationally are the lenders who could have given fixed-rate mortgages but persuaded many people to take variable-rate loans which then turned sour, often containing verbal promises to turn the mortgages later into fixed-rate deals (which were lies)....For even educated people, understanding the terms of a mortgage are almost impossible. I am convinced that lobbyists for financial institutions made the contract language confusing....Next, consider Fannie May and Freddie Whatever. McCain blames them and Obama but consider the facts. While these two companies are huge, they are responsible only for 2% to 3% of the housing and mortgage disasters. And McCain's Rick Davis was chief lobbyist for Fannie Mae, receiving big bucks until one month ago.....But the real reason for the financial crisis is more with the packaged fiancial instruments that Wall Street sold around the world. Nobody--even the big guys--understands what the contents of these really are. My son....says even the sophisticated bankers do not. Blame the Congress (Republicans for 6 of the last 8 years), lobbyists and McCain for sticking to deregulation, and the phony "greed" mantra (as tough it is 100% Wall Street's fault now). The Dems are in for some of the blame but the root of all this goes back to Reagan and the start of deregulation....To quote McCain of two or three years ago, "Deregulation is good for the growth of our economy."

To this email I responsed as follows:

As they say, “The Road to Hell is Paved With Good Intentions”.

We are currently in the eye of the storm.

And yes, no one understands these collateralized debt obligations (CDOs) which were backed by asset and mortgage backed securities, because each contains pieces of thousands of mortgages, the true value and rating of which is unknown and would be difficult to determine.

The math was faulty; when constructing these financial instruments the failure or default rate for new non-collateral mortgages (0% down, no income, no asset “liar” mortgages) were assumed to be identical to “normal” or collateral (20% down) mortgages. This is of course ridiculous.

As I see it, the big failure was the ratings agencies. They gave these dubious instruments a rating identical to US Treasury bills and bonds. That is gross negligence. And yes, I do agree that they could not determine some of the underlying numbers. However, it is illogical to assume that a CDO or mortgage based security built from tranches (slices or pieces) of mortgages including sub-prime, sub-sub prime and so on, is as safe as a US Treasury bill and to rate them as such.

There have been a lot of articles alluding to this for the past several years. They were generally given titles such as “the disconnect of return to risk” and so on.

As has been said, there is more than enough blame to go around. Many politicians were eager to get the poor into their own homes; as is the case with many things, this is OK as long as the make-up is a very small percentage of the total mortgages. In the current “crisis”, the total number of houses sold included too many risky mortgages. As a consequence, we today have millions of people in homes they cannot afford to live in, or soon will not be able to afford to live in.

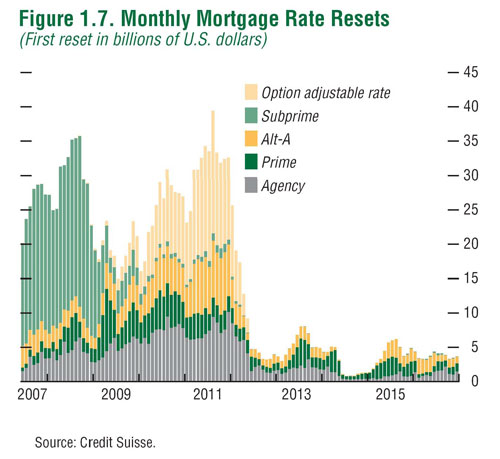

This is so because of the vast quantity of option-ARM loans out there. It is my understanding that these reset five years following the origination of the loan. However, these loans include a clause and if the borrower reaches a specific negative equity, somewhere in the range of 110% to 125% of the original loan balance, then the loan immediately resets to a higher rate. This some call a “surprise” reset. This event is automatic. It is anticipated that many option-ARM borrowers will face significantly higher monthly payment increases in the near future. How many? I saw a chart and it indicated loans totaling about $30 billion will reset in 2009 and as much at $70 billion will reset in 2010. These are not sub-prime loans.

As a result, defaults are expected to double again. Politicians or economists who expect the housing market crises will “bottom” in early 2009 are absolutely wrong, unless there is strong government intervention to prevent these automatic resets. This event is not a surprise. In March 2008, Goldman Sachs estimated that a 15% decline in housing values would occur and that 21% of the total number of people with a mortgage would owe more than their house was worth. However, it was also estimated that if a recession occurred then there would be a total decline in the value of housing of 30% and a whopping 39% of people owing mortgages would be under water. It is now a certainty that we are in or are entering a serious recession.

I am not certain if our government will intervene until it is too late. At present, congress is working on committees of lynching parties rather than averting this looming crisis. So batten down the hatches and be prepared for a potentially rough ride for the next two or three years.

Here is a chart to support what I said about loan resets:

http://www.goodevalue.com/wp-content/uploads/2008/04/imfresets.jpg

As for the “greed”, there are too many questions about that. Is it “greed” to expect to have things I cannot afford? Is it “greed” to expect to live in a house I cannot afford? Is it “greed” to want all of this stuff to the point that we feel entitled to our desires? When every man, woman and child in a nation expects that things will always turn out and that they can and will have in their lifetime whatever they want, at the expense of others, is that “greed”? Or simply stupidity?

{kind=link}

Subscribe to:

Post Comments (Atom)

No comments:

Post a Comment