Back in June 2004 I wrote this:

"I am certain that, given enough time, our brilliant political leaders will screw this up, just as they have all the other social engineering initiatives. (For example, Dick Daley was backpedaling the "Service Economy" at the National Design Engineering and Manufacturing Show, and gave a keynote rally about manufacturing in the USA. Unfortunately, all the exhibitors at the predominant "Southeast Asia", "China", and "Mexico" pavilions, could have cared less!).

"I will be given a permanent "vacation". I just hope I am able to salt enough away to live on while on my furlough and pay for my insurance and all the benefits I will not be entitled to while working during my golden years at Wal-mart. Who knows, the best is yet to come! An alternative from the "If you can’t lick them, join them" Department: become a politician. Just one term in Congress and I get retirement benefits for life, which can't be raided, as can the Social Security "tax" fund".

Showing posts with label The economy. Show all posts

Showing posts with label The economy. Show all posts

Monday, November 17, 2008

Friday, November 7, 2008

Post Election Blues

Well, the presidential election and the primaries are finally over. The Democrats even let Joe Biden out from under his rock, after a time out for bad behavior. I'm sure he's glad to be back.

Note the catchy title. I chose it to honor the color of the party of the winning candidate. Clever, yes?

So now the economists are predicting a deeper than usual recession. Aren't those the same guys and gals who didn't even see most of this coming? So I should listen to them? I think not. I'll continue my own research, and I'll post my conclusions from time to time.

As for the Obama button toter's, I saw this statement by a fan in a WSJ Forum:

"I believe the market will begin to turnaround in the upcoming weeks. President - Elect Obama will lift the spirits of people worldwide, and American Iconic companies such as Coke, Johnson and Johnson, Wal - Mart, etc. will lead the way. The market needed to contract, and shake out the casino/stock analyst. Wall street will regain its stride, as the market starts to respond the worldwide support for American goods. What we have learned is that the American Presidency is more than just a title, it is the measure of the Free - Market. When people believe that the American president is a good person, they respond by buying up American goods".

OK, pass the guy some more cool-aid.

The Onion had a piece on the emptiness facing these people, now that the party is over. What will they do? Maybe go to an orgy in the dorm, or plan an overthrow of some democracy. Is South Korea on the list? Of course, after proposition 8 in California, there is always the Mormon Church to attack. With the power of the web, the opportunities are endless! Onion Video.

To be serious for a moment, I am concerned by the naivete of some of these people. I'm glad they feel good, but feeling good and having confidence is not the same thing. Nothing has really happened yet. We don't even have President elect Obama's design for tackling the problems or a team to do it. In fact, the only thing we do have is most of the same congresswomen and men who got us into this mess in the first place. Wake up America!

The economy will turn around when people again have confidence in the economy. It will turn around when they reach the point that they are certain that a depression is not just around the corner, or if one has arrived, that we have survived it; and when they reach the point that they can trust their money in the stock market, and in the banks. Finally, it will turn around when the herd reaches the point at which they feel secure. We have a long way to go before the guy or gal in the street feels that way. At present, millions have seen a large chunk of their savings vaporize (or someone else's in the case of many home "owners"). However, it is very important to remember that the stock market will turn around before the economy does. So if you see the stock market turning up and staying there, that's a good sign. As for the economy, it will be a year or more before it actually bottoms. That's my guess, sometime late 2009 or early 2010. Sorry to all of you "instant gratification" people out there. Remember, the crazy people, the speculators, have been out of the asylum and running the financial system for a few years. It's going to take a while to clean up the mess they created. If you were flipping houses, or bought one in 2006-7 and expected a huge increase in value, you should be aware I am talking about people just like you!

I'll know the worst is over when the retirees climb out of their homes and into the light of day and again begin purchasing dinner at the diner down the street. At present, many of these people have apparently, like the proverbial turtle, pulled their head in and dug down. One local restaurant which these types frequent, told me their business was off 70%! Who knows when they will return? Perhaps they'll climb up into the sunlight with the return of spring, or when they begin feeling flush with the 5.8% SS benefit increase. Those retirees and other beneficiaries have a big impact on the economy. As of September, 2008 they numbered over 50 million! See Social Security Beneficiaries Snapshot. To put this number in perspective, in 2006, according to the US Census bureau, there were 144 million employed civilian workers in the US. See US Census Employed Civilians. So when the social security beneficiaries pull back, about 26% of the population with income pulls it's chips off the table. As some of these people work and collect benefits, there is possibly a larger effect on the economy.

For many of us, who have never experienced a true, deep recession, this is a new phenomenon. Unlike the "worst recession since the great depression" campaign rhetoric that Sen. Kerry used in his bid for the presidency, this is the real deal. Kerry was spouting bull. I do remember the Arab oil embargo, the recessions of 1973-74, 1980-82, and the stock market crash of 1987. I have been in the work force since 1963 (worked a real job in high school) so this is not a shock to me. However, it isn't pleasant, either. Now we have to deal with those around us who did not prepare, who refused to prepare, or who speculated and gambled, and deal with the fact that "People Will Be Strange."

Now everyone is impatient to get beyond this crisis. Heck, the unemployment numbers have just begun to really rise. It will take time for this to be resolved, and until then, we can only watch and deal with our personal realities. It took years to get into this mess. It will take years to get out of it. As I said earlier in this blog, we could bottom out in late 2009. But that means that at that point we are just beginning to claw our way out of the pit. If you don't believe me then do your own research, but do avoid MSNBC and the other minute miracle entertainers out there. And don't believe anything an economist or politician tells you.

Nor do we know what will be at the end of the tunnel when we do emerge. Given the typical Americans penchant for instant gratification, I have no idea on how these addicts will deal with the new reality. I do know that some and perhaps many of us will eventually come to the conclusion that the worst is over, and like the passing of a tornado, we will conclude it is safe to again emerge from our shelters. At that point we will breath a sigh of relief and allow our lives to resume. When enough of us have done this, the stock market will begin a reversal, people will begin spending some of the cash they hoarded during the "crisis" and the economy will rebound. Will we return to the "good old days" of the Internet boom, cheap credit and so on? No. We blew that wad of cash and sent much of it overseas. Nor will oil return to $25 a barrel; more likely it will return to $150 a barrel and continue upwards, perhaps reaching the predicted $200 a barrel in 2030.

Until then, I suggest we simply watch something besides the talking heads, the economists and that drivelling weatherman Tom Skilling on WGN-TV. Unless you enjoy the equivalent to listening to our economists. You know, 15 minutes of noise about the weather, and then the next morning no matter what Skilling said, you look out the window, go online to Weather.com and decide how to deal with the current events. As for TS's Proselytizing, as we know, the weather will do what it will do, and frequently, it has little to do with the "predictions".

On a positive note about the election, Pres. elect Obama may be the perfect guy for the job. Let him deal with his team-mates Nancy Pelosi, Harry Reid, Charles Rangel, John Dingell, Barney Frank and the rest of them. Have fun fella! This will be more entertaining to watch than the weather or the economists. Of that, I am absolutely certain. The trick will be to separate the wheat from the chaff.

Today, the New York Times decided to put a positive spin on the economy in the article:

Stocks Are Higher After Jobs Report. Here are a couple of choice quotes:

"Investors were not letting a barrage of grim economic news get them down.......After two days of heavy losses, shares on Wall Street bounced back on Friday................In late afternoon trading, the Dow industrials were up about 165 points............but they were still poised to close lower for the week after a two-day sell-off that sent the Dow plunging by nearly 1,000 points".

Ok, so this cool-aid would have me celebrating that the Dow is only down 835 points, or about 9% over the past three days. Wow, I am thrilled. If I had put $10,000 into the market at the close on Wednesday, I would have lost "only" about $710 by the close on Friday; it was actually a larger loss at the time the NYT issued their "news". That's what they call "bouncing back" in New York ? I'm sure my broker would be thrilled, as he made a commission on the sale. Oh, that's right, Wall Street is in New York City, isn't it? So my stock purchase was good for the big, rotten apple. Should I send some more $$$ to the poor people in Times Square? I think not! OK, to put a positive spin on all of this, as they say "long term" the stock market indexes always go up! However, brokers make no money selling Vanguard indexes, so it is some company's stock I would have purchased. In 5 years or so, my stock may be worth more than I paid for it, or then again, the company could have imploded, like Enron!

Note the catchy title. I chose it to honor the color of the party of the winning candidate. Clever, yes?

So now the economists are predicting a deeper than usual recession. Aren't those the same guys and gals who didn't even see most of this coming? So I should listen to them? I think not. I'll continue my own research, and I'll post my conclusions from time to time.

As for the Obama button toter's, I saw this statement by a fan in a WSJ Forum:

"I believe the market will begin to turnaround in the upcoming weeks. President - Elect Obama will lift the spirits of people worldwide, and American Iconic companies such as Coke, Johnson and Johnson, Wal - Mart, etc. will lead the way. The market needed to contract, and shake out the casino/stock analyst. Wall street will regain its stride, as the market starts to respond the worldwide support for American goods. What we have learned is that the American Presidency is more than just a title, it is the measure of the Free - Market. When people believe that the American president is a good person, they respond by buying up American goods".

OK, pass the guy some more cool-aid.

The Onion had a piece on the emptiness facing these people, now that the party is over. What will they do? Maybe go to an orgy in the dorm, or plan an overthrow of some democracy. Is South Korea on the list? Of course, after proposition 8 in California, there is always the Mormon Church to attack. With the power of the web, the opportunities are endless! Onion Video.

To be serious for a moment, I am concerned by the naivete of some of these people. I'm glad they feel good, but feeling good and having confidence is not the same thing. Nothing has really happened yet. We don't even have President elect Obama's design for tackling the problems or a team to do it. In fact, the only thing we do have is most of the same congresswomen and men who got us into this mess in the first place. Wake up America!

The economy will turn around when people again have confidence in the economy. It will turn around when they reach the point that they are certain that a depression is not just around the corner, or if one has arrived, that we have survived it; and when they reach the point that they can trust their money in the stock market, and in the banks. Finally, it will turn around when the herd reaches the point at which they feel secure. We have a long way to go before the guy or gal in the street feels that way. At present, millions have seen a large chunk of their savings vaporize (or someone else's in the case of many home "owners"). However, it is very important to remember that the stock market will turn around before the economy does. So if you see the stock market turning up and staying there, that's a good sign. As for the economy, it will be a year or more before it actually bottoms. That's my guess, sometime late 2009 or early 2010. Sorry to all of you "instant gratification" people out there. Remember, the crazy people, the speculators, have been out of the asylum and running the financial system for a few years. It's going to take a while to clean up the mess they created. If you were flipping houses, or bought one in 2006-7 and expected a huge increase in value, you should be aware I am talking about people just like you!

I'll know the worst is over when the retirees climb out of their homes and into the light of day and again begin purchasing dinner at the diner down the street. At present, many of these people have apparently, like the proverbial turtle, pulled their head in and dug down. One local restaurant which these types frequent, told me their business was off 70%! Who knows when they will return? Perhaps they'll climb up into the sunlight with the return of spring, or when they begin feeling flush with the 5.8% SS benefit increase. Those retirees and other beneficiaries have a big impact on the economy. As of September, 2008 they numbered over 50 million! See Social Security Beneficiaries Snapshot. To put this number in perspective, in 2006, according to the US Census bureau, there were 144 million employed civilian workers in the US. See US Census Employed Civilians. So when the social security beneficiaries pull back, about 26% of the population with income pulls it's chips off the table. As some of these people work and collect benefits, there is possibly a larger effect on the economy.

For many of us, who have never experienced a true, deep recession, this is a new phenomenon. Unlike the "worst recession since the great depression" campaign rhetoric that Sen. Kerry used in his bid for the presidency, this is the real deal. Kerry was spouting bull. I do remember the Arab oil embargo, the recessions of 1973-74, 1980-82, and the stock market crash of 1987. I have been in the work force since 1963 (worked a real job in high school) so this is not a shock to me. However, it isn't pleasant, either. Now we have to deal with those around us who did not prepare, who refused to prepare, or who speculated and gambled, and deal with the fact that "People Will Be Strange."

Now everyone is impatient to get beyond this crisis. Heck, the unemployment numbers have just begun to really rise. It will take time for this to be resolved, and until then, we can only watch and deal with our personal realities. It took years to get into this mess. It will take years to get out of it. As I said earlier in this blog, we could bottom out in late 2009. But that means that at that point we are just beginning to claw our way out of the pit. If you don't believe me then do your own research, but do avoid MSNBC and the other minute miracle entertainers out there. And don't believe anything an economist or politician tells you.

Nor do we know what will be at the end of the tunnel when we do emerge. Given the typical Americans penchant for instant gratification, I have no idea on how these addicts will deal with the new reality. I do know that some and perhaps many of us will eventually come to the conclusion that the worst is over, and like the passing of a tornado, we will conclude it is safe to again emerge from our shelters. At that point we will breath a sigh of relief and allow our lives to resume. When enough of us have done this, the stock market will begin a reversal, people will begin spending some of the cash they hoarded during the "crisis" and the economy will rebound. Will we return to the "good old days" of the Internet boom, cheap credit and so on? No. We blew that wad of cash and sent much of it overseas. Nor will oil return to $25 a barrel; more likely it will return to $150 a barrel and continue upwards, perhaps reaching the predicted $200 a barrel in 2030.

Until then, I suggest we simply watch something besides the talking heads, the economists and that drivelling weatherman Tom Skilling on WGN-TV. Unless you enjoy the equivalent to listening to our economists. You know, 15 minutes of noise about the weather, and then the next morning no matter what Skilling said, you look out the window, go online to Weather.com and decide how to deal with the current events. As for TS's Proselytizing, as we know, the weather will do what it will do, and frequently, it has little to do with the "predictions".

On a positive note about the election, Pres. elect Obama may be the perfect guy for the job. Let him deal with his team-mates Nancy Pelosi, Harry Reid, Charles Rangel, John Dingell, Barney Frank and the rest of them. Have fun fella! This will be more entertaining to watch than the weather or the economists. Of that, I am absolutely certain. The trick will be to separate the wheat from the chaff.

Today, the New York Times decided to put a positive spin on the economy in the article:

Stocks Are Higher After Jobs Report. Here are a couple of choice quotes:

"Investors were not letting a barrage of grim economic news get them down.......After two days of heavy losses, shares on Wall Street bounced back on Friday................In late afternoon trading, the Dow industrials were up about 165 points............but they were still poised to close lower for the week after a two-day sell-off that sent the Dow plunging by nearly 1,000 points".

Ok, so this cool-aid would have me celebrating that the Dow is only down 835 points, or about 9% over the past three days. Wow, I am thrilled. If I had put $10,000 into the market at the close on Wednesday, I would have lost "only" about $710 by the close on Friday; it was actually a larger loss at the time the NYT issued their "news". That's what they call "bouncing back" in New York ? I'm sure my broker would be thrilled, as he made a commission on the sale. Oh, that's right, Wall Street is in New York City, isn't it? So my stock purchase was good for the big, rotten apple. Should I send some more $$$ to the poor people in Times Square? I think not! OK, to put a positive spin on all of this, as they say "long term" the stock market indexes always go up! However, brokers make no money selling Vanguard indexes, so it is some company's stock I would have purchased. In 5 years or so, my stock may be worth more than I paid for it, or then again, the company could have imploded, like Enron!

Wednesday, October 22, 2008

Ask me in 20 Years!

I was asked recently if I am invested in the stock market. That question was prompted by our recent financial "crisis" and the current aftermath. The answer is YES! Here are my reasons:

- Both my spouse and I are employed. We do save a portion of our earnings each month and a substantial portion of these savings goes into retirement accounts.

- We are of an age where it is likely one of us will still be on this planet in 40 years. Look at it this way. Consider that today it is the year 1968 and that one of us will probably still be on the planet in the year 2008! From the perspective of 1968, that's a long, long way into the future. A lot can happen in 40 years, and probably will. For example, there were seven (7) bear or near bear markets in that period, including the "bear market of 2008-2009". So we need a financial plan which can accomodate that unknowable, somewhat distant future.

- Inflation is a long term concern.

- There is evidence that the stock market is a good hedge against inflation, over the long term.

- That portion of the funds we do have "invested" are in a diversified portfolio. That portfolio is somewhat conservative and includes dividend paying stocks, mutual funds and bonds.

- We are applying the principle of dividend reinvestment. Dividend yields are highest when the stock market is at the bottom, and dividend reinvestment ensures that new shares are purchased at these lower prices. In the super- or mega-bear market of 1773-74 and during the ensuing malaise when stock market indexes were flat for nearly 10 years, there were dividend yields of up to 5%. Those yields enabled substantially better total returns than the market indexes would suggest.

- We have some funds, including an "emergency fund" which are not invested in the stock market and we can tolerate waiting 10 years for a market return.

- We are doing our best to maintain a long term focus.

- We are aware there are risks. There is always the unknowable. It is possible neither of us will be alive in 5 years. It is also possible that we will both be alive in 40 years. So we do our best to plan for both possibilities.

So that is our rationale. On the other hand, it isn't easy watching the government hand over $$ of our taxes to the banks and investment bankers who contributed to this mess. Nor is it easy listening to the whining of those who want to help the "poor homeowners". Many of those "poor homeowners" were as greedy as the bankers who got us into this mess. I suppose some sort of intervention will be necessary. There are rational arguments both for and against. I suspect that the financial turmoil will not end until the housing market is stabilized. One good thing, "Wall Street" has finally gotten the "black eye" it has deserved! No matter who is elected as President in 2008, there will be some change in the way that Wall Street is treated in America.

I think it is important to seperate the housing problems from the economy at large. I don't know how people will adjust to the reality of the new credit landscape. The worst could be over in 6 months. However, I do think it will take years to sort some of this out, and that home prices will fall for perhaps 5 years or until 2013. That will not necessarily be universal, as "all real estate is local" as the saying goes. However, California in particular will have many single-family homes priced below their peak levels of 2006-2007. Home valuations in the hardest hit areas will probably be 50% of their peak value. This is not my SWAG here, I am presenting numbers I have distilled from many sources.

As the economy stabilizes and panic recedes, many people will realize that things aren't as bad as they thought they would be. The stock market will recover. In particular, there will be a need to invest and as housing will no longer be the rock star it once was, the stock market may be considered a reasonable place for such investments. I base this optimism on the recent past, most notably the aftermath of the internet boom and bust of 2002.

When I was asked "why am I invested in the stock market", the question could as easily have been "why am I invested in America?", for that is what I am doing. I have always had a faith in the ability of this amazing country to transcend certain problems and idiosyncrasies of human beings. However, the past 10 years have been trying, and have tested that faith. Should I be concerned? Yes, I think I should be! Should I panic? No, and to help me in that I will attempt to watch as little financial news as possible. (Note: keeping these blogs going and minimizing exposure is going to be a task; I'll definitely be avoiding most of the "popular" media and as many of the "talking heads" as possible).

One other thing I keep in mind. A lot of the financial news is generated in New York and as we know, that town is tightening it's belt and looking toward gloomier times. I am of the opinion that this will cloud the news emanating from that city. Consider it an internal bias to the news. I will be listening for that bias.

The bottom line: Have I made good decisions? How will it turn out? Ask me in 10 to 20 years!

PS: I know that the conventional wisdom is oil and other consumables will tank in a recession, or a serious recession. However, I couldn't pass up the opportunity to pick up some National Oilwell Varco (NOV)

Monday, October 20, 2008

Was it Greed or Stupidity?

I saw an article on Henry Cisneros, Clinton's Top Housing Official. He now has some misgivings about the housing market:

http://www.nytimes.com/2008/10/19/business/19cisneros.html?_r=1&em&oref=slogin

I sent the article on to a friend with some comments. He replied with an email "Thanks for sending the article which I missed in my rush thru the day. I always thought he [Cisneros] was a bad guy, starting from the sex scandal and what I read about him....He is partly to blame. And there are zillions of others....In the housing disaster, more to blame nationally are the lenders who could have given fixed-rate mortgages but persuaded many people to take variable-rate loans which then turned sour, often containing verbal promises to turn the mortgages later into fixed-rate deals (which were lies)....For even educated people, understanding the terms of a mortgage are almost impossible. I am convinced that lobbyists for financial institutions made the contract language confusing....Next, consider Fannie May and Freddie Whatever. McCain blames them and Obama but consider the facts. While these two companies are huge, they are responsible only for 2% to 3% of the housing and mortgage disasters. And McCain's Rick Davis was chief lobbyist for Fannie Mae, receiving big bucks until one month ago.....But the real reason for the financial crisis is more with the packaged fiancial instruments that Wall Street sold around the world. Nobody--even the big guys--understands what the contents of these really are. My son....says even the sophisticated bankers do not. Blame the Congress (Republicans for 6 of the last 8 years), lobbyists and McCain for sticking to deregulation, and the phony "greed" mantra (as tough it is 100% Wall Street's fault now). The Dems are in for some of the blame but the root of all this goes back to Reagan and the start of deregulation....To quote McCain of two or three years ago, "Deregulation is good for the growth of our economy."

To this email I responsed as follows:

As they say, “The Road to Hell is Paved With Good Intentions”.

We are currently in the eye of the storm.

And yes, no one understands these collateralized debt obligations (CDOs) which were backed by asset and mortgage backed securities, because each contains pieces of thousands of mortgages, the true value and rating of which is unknown and would be difficult to determine.

The math was faulty; when constructing these financial instruments the failure or default rate for new non-collateral mortgages (0% down, no income, no asset “liar” mortgages) were assumed to be identical to “normal” or collateral (20% down) mortgages. This is of course ridiculous.

As I see it, the big failure was the ratings agencies. They gave these dubious instruments a rating identical to US Treasury bills and bonds. That is gross negligence. And yes, I do agree that they could not determine some of the underlying numbers. However, it is illogical to assume that a CDO or mortgage based security built from tranches (slices or pieces) of mortgages including sub-prime, sub-sub prime and so on, is as safe as a US Treasury bill and to rate them as such.

There have been a lot of articles alluding to this for the past several years. They were generally given titles such as “the disconnect of return to risk” and so on.

As has been said, there is more than enough blame to go around. Many politicians were eager to get the poor into their own homes; as is the case with many things, this is OK as long as the make-up is a very small percentage of the total mortgages. In the current “crisis”, the total number of houses sold included too many risky mortgages. As a consequence, we today have millions of people in homes they cannot afford to live in, or soon will not be able to afford to live in.

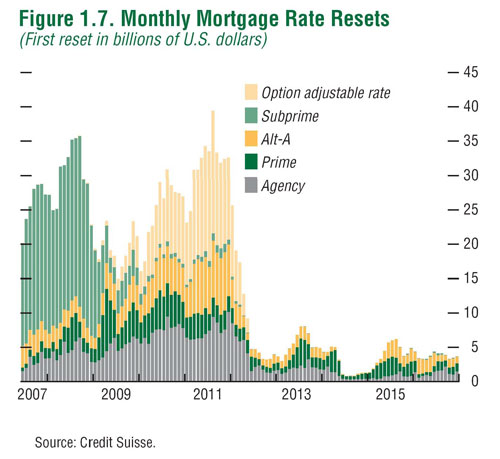

This is so because of the vast quantity of option-ARM loans out there. It is my understanding that these reset five years following the origination of the loan. However, these loans include a clause and if the borrower reaches a specific negative equity, somewhere in the range of 110% to 125% of the original loan balance, then the loan immediately resets to a higher rate. This some call a “surprise” reset. This event is automatic. It is anticipated that many option-ARM borrowers will face significantly higher monthly payment increases in the near future. How many? I saw a chart and it indicated loans totaling about $30 billion will reset in 2009 and as much at $70 billion will reset in 2010. These are not sub-prime loans.

As a result, defaults are expected to double again. Politicians or economists who expect the housing market crises will “bottom” in early 2009 are absolutely wrong, unless there is strong government intervention to prevent these automatic resets. This event is not a surprise. In March 2008, Goldman Sachs estimated that a 15% decline in housing values would occur and that 21% of the total number of people with a mortgage would owe more than their house was worth. However, it was also estimated that if a recession occurred then there would be a total decline in the value of housing of 30% and a whopping 39% of people owing mortgages would be under water. It is now a certainty that we are in or are entering a serious recession.

I am not certain if our government will intervene until it is too late. At present, congress is working on committees of lynching parties rather than averting this looming crisis. So batten down the hatches and be prepared for a potentially rough ride for the next two or three years.

Here is a chart to support what I said about loan resets:

http://www.goodevalue.com/wp-content/uploads/2008/04/imfresets.jpg

As for the “greed”, there are too many questions about that. Is it “greed” to expect to have things I cannot afford? Is it “greed” to expect to live in a house I cannot afford? Is it “greed” to want all of this stuff to the point that we feel entitled to our desires? When every man, woman and child in a nation expects that things will always turn out and that they can and will have in their lifetime whatever they want, at the expense of others, is that “greed”? Or simply stupidity?

http://www.nytimes.com/2008/10/19/business/19cisneros.html?_r=1&em&oref=slogin

I sent the article on to a friend with some comments. He replied with an email "Thanks for sending the article which I missed in my rush thru the day. I always thought he [Cisneros] was a bad guy, starting from the sex scandal and what I read about him....He is partly to blame. And there are zillions of others....In the housing disaster, more to blame nationally are the lenders who could have given fixed-rate mortgages but persuaded many people to take variable-rate loans which then turned sour, often containing verbal promises to turn the mortgages later into fixed-rate deals (which were lies)....For even educated people, understanding the terms of a mortgage are almost impossible. I am convinced that lobbyists for financial institutions made the contract language confusing....Next, consider Fannie May and Freddie Whatever. McCain blames them and Obama but consider the facts. While these two companies are huge, they are responsible only for 2% to 3% of the housing and mortgage disasters. And McCain's Rick Davis was chief lobbyist for Fannie Mae, receiving big bucks until one month ago.....But the real reason for the financial crisis is more with the packaged fiancial instruments that Wall Street sold around the world. Nobody--even the big guys--understands what the contents of these really are. My son....says even the sophisticated bankers do not. Blame the Congress (Republicans for 6 of the last 8 years), lobbyists and McCain for sticking to deregulation, and the phony "greed" mantra (as tough it is 100% Wall Street's fault now). The Dems are in for some of the blame but the root of all this goes back to Reagan and the start of deregulation....To quote McCain of two or three years ago, "Deregulation is good for the growth of our economy."

To this email I responsed as follows:

As they say, “The Road to Hell is Paved With Good Intentions”.

We are currently in the eye of the storm.

And yes, no one understands these collateralized debt obligations (CDOs) which were backed by asset and mortgage backed securities, because each contains pieces of thousands of mortgages, the true value and rating of which is unknown and would be difficult to determine.

The math was faulty; when constructing these financial instruments the failure or default rate for new non-collateral mortgages (0% down, no income, no asset “liar” mortgages) were assumed to be identical to “normal” or collateral (20% down) mortgages. This is of course ridiculous.

As I see it, the big failure was the ratings agencies. They gave these dubious instruments a rating identical to US Treasury bills and bonds. That is gross negligence. And yes, I do agree that they could not determine some of the underlying numbers. However, it is illogical to assume that a CDO or mortgage based security built from tranches (slices or pieces) of mortgages including sub-prime, sub-sub prime and so on, is as safe as a US Treasury bill and to rate them as such.

There have been a lot of articles alluding to this for the past several years. They were generally given titles such as “the disconnect of return to risk” and so on.

As has been said, there is more than enough blame to go around. Many politicians were eager to get the poor into their own homes; as is the case with many things, this is OK as long as the make-up is a very small percentage of the total mortgages. In the current “crisis”, the total number of houses sold included too many risky mortgages. As a consequence, we today have millions of people in homes they cannot afford to live in, or soon will not be able to afford to live in.

This is so because of the vast quantity of option-ARM loans out there. It is my understanding that these reset five years following the origination of the loan. However, these loans include a clause and if the borrower reaches a specific negative equity, somewhere in the range of 110% to 125% of the original loan balance, then the loan immediately resets to a higher rate. This some call a “surprise” reset. This event is automatic. It is anticipated that many option-ARM borrowers will face significantly higher monthly payment increases in the near future. How many? I saw a chart and it indicated loans totaling about $30 billion will reset in 2009 and as much at $70 billion will reset in 2010. These are not sub-prime loans.

As a result, defaults are expected to double again. Politicians or economists who expect the housing market crises will “bottom” in early 2009 are absolutely wrong, unless there is strong government intervention to prevent these automatic resets. This event is not a surprise. In March 2008, Goldman Sachs estimated that a 15% decline in housing values would occur and that 21% of the total number of people with a mortgage would owe more than their house was worth. However, it was also estimated that if a recession occurred then there would be a total decline in the value of housing of 30% and a whopping 39% of people owing mortgages would be under water. It is now a certainty that we are in or are entering a serious recession.

I am not certain if our government will intervene until it is too late. At present, congress is working on committees of lynching parties rather than averting this looming crisis. So batten down the hatches and be prepared for a potentially rough ride for the next two or three years.

Here is a chart to support what I said about loan resets:

http://www.goodevalue.com/wp-content/uploads/2008/04/imfresets.jpg

{kind=link}

As for the “greed”, there are too many questions about that. Is it “greed” to expect to have things I cannot afford? Is it “greed” to expect to live in a house I cannot afford? Is it “greed” to want all of this stuff to the point that we feel entitled to our desires? When every man, woman and child in a nation expects that things will always turn out and that they can and will have in their lifetime whatever they want, at the expense of others, is that “greed”? Or simply stupidity?

Tuesday, September 16, 2008

More on "Change"

Well, we wanted "change" and it seems we are getting it. Just four years ago, Senator Kerry was out there stumping his candidacy and telling us that it "was the worst economy since the great depression". I guess he was a little early, or prescient. But by golly, he was correct. Or maybe if you make sufficient predictions, eventually they will all come true. Eventually, the world will end and if you flip a coin you will eventually get "heads".

NY Mayor Bloomberg was talking to the media and calming the waters. He said that "New York is as well prepared as ever to handle the financial emergency" or words to that effect. He has cause to worry. For every job lost on Wall Street about 2 or 3 dependent jobs are also lost. And as we know from the screaming headlines of the past few years, these were not "ordinary" jobs, as in "median income". These are high rollers, who spend a lot of money on toys, dining out and so on. The State Comptroller's office in New York has been quoted as stating that approximately 5% of the jobs in New York City's jobs are in financial services. However, those jobs account for about 25% of the city's wages. That was $60 billion in 2006.

I haven't heard a word from New York's Senator Clinton on all of this. But it could simply be that the media is so inundated with bad news that they simply won't give her any air time. The Senator has had a field day bashing the "oil companies" because of their excess profits. I have been waiting for her to bash Wall Street for it's inordinate greed, profiteering, etc. Since 2007 Americans have lost $2 trillion dollars as a result of the "sub prime" and "prime" meltdown. That makes a few billion in profits for the oil companies look like chump change.

http://letmethinkaboutthis.blogspot.com/2008/09/some-musings-on-economy.html

Besides, it isn't like I am getting nothing from the refiners. To the contrary, I fill up my gas tank whenever necessary and we as in "we Americans" send about $500 to $700 billion each year to legitimate and despotic governments all over the world, because we can't or won't stop our insatiable desire for oil.

Oh, and let's not forget, this is all a choice. We choose not to drill, we choose to drive SUV's and we choose to drive trillions of miles each year.

Wall Street, the banks and the politicians are in collusion to steal our money. Now we have low interest rates so as to prop up the banks on Wall Street (again) which means retirees are hard pressed to get a decent return on their money in CDs or bank accounts. To get a return, it seems, we are supposed to invest in unsafe, unregulated financial instruments. And who decided that? Thank you all, including Senator Clinton for your silence and lack of action. We know whose pocket you are in!

NY Mayor Bloomberg was talking to the media and calming the waters. He said that "New York is as well prepared as ever to handle the financial emergency" or words to that effect. He has cause to worry. For every job lost on Wall Street about 2 or 3 dependent jobs are also lost. And as we know from the screaming headlines of the past few years, these were not "ordinary" jobs, as in "median income". These are high rollers, who spend a lot of money on toys, dining out and so on. The State Comptroller's office in New York has been quoted as stating that approximately 5% of the jobs in New York City's jobs are in financial services. However, those jobs account for about 25% of the city's wages. That was $60 billion in 2006.

I haven't heard a word from New York's Senator Clinton on all of this. But it could simply be that the media is so inundated with bad news that they simply won't give her any air time. The Senator has had a field day bashing the "oil companies" because of their excess profits. I have been waiting for her to bash Wall Street for it's inordinate greed, profiteering, etc. Since 2007 Americans have lost $2 trillion dollars as a result of the "sub prime" and "prime" meltdown. That makes a few billion in profits for the oil companies look like chump change.

http://letmethinkaboutthis.blogspot.com/2008/09/some-musings-on-economy.html

Besides, it isn't like I am getting nothing from the refiners. To the contrary, I fill up my gas tank whenever necessary and we as in "we Americans" send about $500 to $700 billion each year to legitimate and despotic governments all over the world, because we can't or won't stop our insatiable desire for oil.

Oh, and let's not forget, this is all a choice. We choose not to drill, we choose to drive SUV's and we choose to drive trillions of miles each year.

Wall Street, the banks and the politicians are in collusion to steal our money. Now we have low interest rates so as to prop up the banks on Wall Street (again) which means retirees are hard pressed to get a decent return on their money in CDs or bank accounts. To get a return, it seems, we are supposed to invest in unsafe, unregulated financial instruments. And who decided that? Thank you all, including Senator Clinton for your silence and lack of action. We know whose pocket you are in!

Tuesday, August 26, 2008

Economic Woes?

Apparently, this will be another sideways day on wall street. Yesterday the market paused on its wayward trip to the gutter. If we keep purchasing stock on the way down, I have been told that is a method of “dollar loss averaging”, with the purpose of spreading the pain out over months and months and providing our stock brokers with much needed revenue..

Thinking of the economy reminds me that it is four years since the last presidential campaign. That’s difficult to believe; seems like it was just yesterday that the Hon. Senator Kerry was stumping his position that it “was the worst economy since the great depression”. I wasn’t around for that depression, so I don’t know. However, I do remember my parents telling me a few stories, such as the one about people walking along the rails in winter, picking up pieces of coal discarded from the trains. This was apparently used to heat homes and for cooking. Sounded plausible to me! When I was a kid growing up in Chicago in the 1950s, we had a coal stove and oven in the kitchen. An explosion in that stove blew the round inserts off of the stove top and into the ceiling. This was attributed to a blasting cap or caps left in the coal. That event stimulated the family’s quest for a more modern fuel. We switched to kerosene and natural gas. The advantage was less ash, but it was still necessary to carry a large can of fuel oil up three flights of stairs twice each day.

But I digress. So the present economy is much worse than it was four years ago. I guess the big question is, how bad will it get? The second questions is “How long will it last?” Well, this is not the first or even the second recession I have experienced. I once experienced very high prime rates that resulted in the interest rate on my second mortgage reaching something like 21%! That was like purchasing a house on a credit card. Ouch! We have a way to go before we get to that point.

I remember watching President Jimmy Carter, sitting in front of a fire place dressed in a neat sweater, telling us all how we were going to have to pay the price for our past sins, or something like that. Well, I don’t know about “we” but I do know I paid a price. Recently, while watching former President Carter on a TV interview, I concluded that he has made out pretty well. Somehow the politicians always seem to make out very well, unless they get caught with their hand in the proverbial cookie jar.

As to how difficult it will be for the rest of us, using history as a guide, it will be unpleasant or worse. We are not yet at the particular day of reckoning for this fiasco (which in Wall Street parlance is the “market bottom”). I expect we’ll be getting close when the mantra “How could this happen?” becomes a din!

As the economy winds down, sales tax revenues will drop. This will impact communities large and small. Of course, our political and civic leaders have spent every last dime and so they are no more prepared for this than the rest of us, who also assumed that the good times would roll on, forever. Apparently we believed that recessions never happen, housing values always go up, inflation is always moderate, energy will forever be cheap, etc., etc., etc. Unfortunately for us, history and reality do not support that rosy lensed view.

Statistics quoted in the media imply that millions of my fellow citizens have spent the past 10 years using their home as an ATM machine so they can support their lifestyle. Feeling strapped by the current housing implosion, they are now turning toward robbing their 401Ks. Of course, home owners and apartment dwellers alike have maxed out their credit cards. My personal solution has been to upgrade my shredder to a near industrial model to keep up with the credit card offers I receive daily. I assume I am average in this.

Waiting for the unraveling and the inevitable bottom is boring, with an edge. It’s like watching the movie Jaws for the 100th time. I hear the music, I know the shark is in the water and I know somebody is going to die. Eventually after the carnage is over, the shark will be slaughtered and the water will again turn blue.

I view our economy to be similar and when the clouds part, the cycle of excess will begin anew.

Until we get to that point, home-livers who are faced with upside down mortgages will be bailing. This will put pressure on many banks and credit unions who provided the mortgages and now are stuck with foreclosures. The Federal Deposit Insurance Corp. announced on August 26 that its list of "problem" banks, or those at risk of failure had grown from 90 three months ago to 117 as of June 30.

I expect the home-livers to bail out for the same reason they jumped into the housing market. Greed! The thought that one could have a house for little or no cost which would turn into a cash machine, was more than many could resist. That same philosophy will get them out of the housing market. Why own something that requires maintenance and cash injections? Having a house was simply an expedient, an opportunistic moment! So how bad it gets for the rest of us, will I think, be determined by how many bail. If everyone who “purchased” a home since 2005 decides to jump ship, leaving the rest of us to clean up the mess, it could get nasty, indeed!

My personal opinion is that it will take a few years for this particular “game” to go around the entire board and return to “home”. So those who are looking forward to quick resolution will be disappointed.

Thinking of the economy reminds me that it is four years since the last presidential campaign. That’s difficult to believe; seems like it was just yesterday that the Hon. Senator Kerry was stumping his position that it “was the worst economy since the great depression”. I wasn’t around for that depression, so I don’t know. However, I do remember my parents telling me a few stories, such as the one about people walking along the rails in winter, picking up pieces of coal discarded from the trains. This was apparently used to heat homes and for cooking. Sounded plausible to me! When I was a kid growing up in Chicago in the 1950s, we had a coal stove and oven in the kitchen. An explosion in that stove blew the round inserts off of the stove top and into the ceiling. This was attributed to a blasting cap or caps left in the coal. That event stimulated the family’s quest for a more modern fuel. We switched to kerosene and natural gas. The advantage was less ash, but it was still necessary to carry a large can of fuel oil up three flights of stairs twice each day.

But I digress. So the present economy is much worse than it was four years ago. I guess the big question is, how bad will it get? The second questions is “How long will it last?” Well, this is not the first or even the second recession I have experienced. I once experienced very high prime rates that resulted in the interest rate on my second mortgage reaching something like 21%! That was like purchasing a house on a credit card. Ouch! We have a way to go before we get to that point.

I remember watching President Jimmy Carter, sitting in front of a fire place dressed in a neat sweater, telling us all how we were going to have to pay the price for our past sins, or something like that. Well, I don’t know about “we” but I do know I paid a price. Recently, while watching former President Carter on a TV interview, I concluded that he has made out pretty well. Somehow the politicians always seem to make out very well, unless they get caught with their hand in the proverbial cookie jar.

As to how difficult it will be for the rest of us, using history as a guide, it will be unpleasant or worse. We are not yet at the particular day of reckoning for this fiasco (which in Wall Street parlance is the “market bottom”). I expect we’ll be getting close when the mantra “How could this happen?” becomes a din!

As the economy winds down, sales tax revenues will drop. This will impact communities large and small. Of course, our political and civic leaders have spent every last dime and so they are no more prepared for this than the rest of us, who also assumed that the good times would roll on, forever. Apparently we believed that recessions never happen, housing values always go up, inflation is always moderate, energy will forever be cheap, etc., etc., etc. Unfortunately for us, history and reality do not support that rosy lensed view.

Statistics quoted in the media imply that millions of my fellow citizens have spent the past 10 years using their home as an ATM machine so they can support their lifestyle. Feeling strapped by the current housing implosion, they are now turning toward robbing their 401Ks. Of course, home owners and apartment dwellers alike have maxed out their credit cards. My personal solution has been to upgrade my shredder to a near industrial model to keep up with the credit card offers I receive daily. I assume I am average in this.

Waiting for the unraveling and the inevitable bottom is boring, with an edge. It’s like watching the movie Jaws for the 100th time. I hear the music, I know the shark is in the water and I know somebody is going to die. Eventually after the carnage is over, the shark will be slaughtered and the water will again turn blue.

I view our economy to be similar and when the clouds part, the cycle of excess will begin anew.

Until we get to that point, home-livers who are faced with upside down mortgages will be bailing. This will put pressure on many banks and credit unions who provided the mortgages and now are stuck with foreclosures. The Federal Deposit Insurance Corp. announced on August 26 that its list of "problem" banks, or those at risk of failure had grown from 90 three months ago to 117 as of June 30.

I expect the home-livers to bail out for the same reason they jumped into the housing market. Greed! The thought that one could have a house for little or no cost which would turn into a cash machine, was more than many could resist. That same philosophy will get them out of the housing market. Why own something that requires maintenance and cash injections? Having a house was simply an expedient, an opportunistic moment! So how bad it gets for the rest of us, will I think, be determined by how many bail. If everyone who “purchased” a home since 2005 decides to jump ship, leaving the rest of us to clean up the mess, it could get nasty, indeed!

My personal opinion is that it will take a few years for this particular “game” to go around the entire board and return to “home”. So those who are looking forward to quick resolution will be disappointed.

Subscribe to:

Comments (Atom)