There is a lot of uncertainty out there, and at this point, one cannot help but question the economic condition of the country. People are beginning to crack. I was mentally prepared for a "typical" bear market, but the stock market blew through that is a few weeks. So that brought me to the threshold of pain faster than I expected. However, I am hanging in there and have re-reviewed my financial plan, and my portfolio. I do have a list of stocks that are currently of great interest to me and I just purchased some NOV. As they say, the price was right.

For some calm, non-emotional advice on what to do now, go to this link: Rick Ferri on "What to do in this current market environment"

You can search for "Rick Ferri" using your favorite search engine, if you want to know more about who he is.

As for the negativity out there, those messages flashing across the screen on CNBC: "IS YOUR MONEY SAFE??" certainly don't help, but then, they are simply intended to keep us glued to the screen. I aso suspect that as the program is being beamed from NYC, that there is a built in "negativity bias". Too bad for the talking heads on the financial shows. Anyone who is sane has to question those people. Only recently Jim Cramer was playing the pied piper of the stock market, then turned on his adoring fans and told everyone to bail: Link to video Oct. 6, 2008: Cramer Says Now is the Time to Bail!

For more on Cramer, see: Link to "Forever the Cynic"

We all feel the pain; even with all the balancing and asset allocation I have done to my retirement portfolio, I am experiencing a paper "loss", or decrease in the value of that portfolio, just as everyone who has any exposure to the stock market has experienced. Index funds tanked. Bond funds were dumped. Etc., etc. This was not unexpected; financial people were flashing "bear market ahead" warnings for months. As a consequence I re-allocated by entire portfolio, that is; the portion that is not in cash. I had gone long on cash, as they say, with the remainder set up for a minimum 5 year and possibly a 10 year horizon. Ultimately, the horizon of my retirement accounts is 30 years.

As you can see, I do have a long term perspective, so even though I am not happy to be with our market and the economy in it's present state, I can take some solace that my time perspective is a long one.

To Quote Warren Buffett (Smart Money, May 1997): "If you aren't willing to own a stock for 10 years, don't even think about owning it for 10 minutes." I don't take this advice to literally mean I should buy all stocks and hold them for 10 years, but rather to buy with the expectation that I be prepared to hold them for 10 years.

I also am well aware that sometimes one can do everything right and still not achieve the desired result. So it is still possible to lose money in stocks and bonds. As the saying goes, there are no guarantees in life, no matter what the pandering politicians tell us.

I do have sympathy for those who expected quick returns from the stock market and invested that way, just as I have sympathy for those who purchased a home recently, expecting to flip it in a year or two. Housing is similar to the stock market. Breakeven on a home purchase is typically 5 years as compared to renting, according to most of the financial analysis I have read, and supported by my own, independent analysis.

As I see it, if we think housing or stocks always go up, we will be disappointed. If we think reversals, when they occur, will always be minor and corrected in a year or so, we will also be disappointed. If we think we can gamble and always win, we will lose, and lose big time. That's the way it is.

"The market, he had learned, was like the sea, to be respected and feared. You sail on its smooth surface on a placid mid-summer day; you were borne along by a favoring breeze; took a pleasant swim in its waters, and basked in the rays of the sun. Or you lolled in the quiet currents and dozed. A cold gust of wind brought you to, sharply — clouds gathered, the sun had gone — there were flashes of lightning and peals of thunder; the ocean was whipped into seething waves; your fragile craft was tossed about by heavy seas that broke over its sides. Half the crew was swept overboard... you were washed upon the shore... naked and exhausted you sank upon the beach, thankful for life itself..." Liars Poker, Rising through the Wreckage on Wall Street, by Michael Lewis Link to Liars Poker at Amazon

Saturday, October 25, 2008

Friday, October 24, 2008

The more Starbucks a country has, the bigger its financial problems

This according to Mr. Daniel Gross, at the website "Slate.com":

The more Starbucks a country has, the bigger its financial problems

"I propose the Starbucks theory of international economics. The higher the concentration of expensive, nautically themed, faux-Italian-branded Frappuccino joints in a country's financial capital, the more likely the country is to have suffered catastrophic financial losses.

It may sound doppio, but work with me. This recent crisis has its roots in the unhappy coupling of a frenzied nationwide real-estate market centered in California, Las Vegas, and Florida, and a nationwide credit mania centered in New York. If you could pick one brand name that personified these twin bubbles, it was Starbucks. The Seattle-based coffee chain followed new housing developments into the suburbs and exurbs, where its outlets became pit stops for real-estate brokers and their clients. It also carpet-bombed the business districts of large cities, especially the financial centers, with nearly 200 in Manhattan alone. Starbucks' frothy treats provided the fuel for the boom, the caffeine that enabled deal jockeys to stay up all hours putting together offering papers for CDOs, and helped mortgage brokers work overtime processing dubious loan documents. Starbucks strategically located many of its outlets on the ground floors of big investment banks. (The one around the corner from the former Bear Stearns headquarters has already closed.)"

Mr. Gross goes on to posit the following:

"My tentative theory: Having a significant Starbucks presence is a pretty significant indicator of the degree of connectedness to the form of highly caffeinated, free-spending capitalism that got us into this mess. It's also a sign of a culture's willingness to abandon traditional norms and ways of doing business (virtually all the countries in which Starbucks has established beachheads have their own venerable coffee-house traditions) in favor of fast-moving American ones. The fact that the company or its local licensee felt there was room for dozens of outlets where consumers would pony up lots of euros, liras, and rials for expensive drinks is also a pretty good indicator that excessive financial optimism had entered the bloodstream. "

The more Starbucks a country has, the bigger its financial problems

"I propose the Starbucks theory of international economics. The higher the concentration of expensive, nautically themed, faux-Italian-branded Frappuccino joints in a country's financial capital, the more likely the country is to have suffered catastrophic financial losses.

It may sound doppio, but work with me. This recent crisis has its roots in the unhappy coupling of a frenzied nationwide real-estate market centered in California, Las Vegas, and Florida, and a nationwide credit mania centered in New York. If you could pick one brand name that personified these twin bubbles, it was Starbucks. The Seattle-based coffee chain followed new housing developments into the suburbs and exurbs, where its outlets became pit stops for real-estate brokers and their clients. It also carpet-bombed the business districts of large cities, especially the financial centers, with nearly 200 in Manhattan alone. Starbucks' frothy treats provided the fuel for the boom, the caffeine that enabled deal jockeys to stay up all hours putting together offering papers for CDOs, and helped mortgage brokers work overtime processing dubious loan documents. Starbucks strategically located many of its outlets on the ground floors of big investment banks. (The one around the corner from the former Bear Stearns headquarters has already closed.)"

Mr. Gross goes on to posit the following:

"My tentative theory: Having a significant Starbucks presence is a pretty significant indicator of the degree of connectedness to the form of highly caffeinated, free-spending capitalism that got us into this mess. It's also a sign of a culture's willingness to abandon traditional norms and ways of doing business (virtually all the countries in which Starbucks has established beachheads have their own venerable coffee-house traditions) in favor of fast-moving American ones. The fact that the company or its local licensee felt there was room for dozens of outlets where consumers would pony up lots of euros, liras, and rials for expensive drinks is also a pretty good indicator that excessive financial optimism had entered the bloodstream. "

Thursday, October 23, 2008

Here Comes Socialism

If you don't think it is coming, in a serious way, then consider this. Today Alan Greenspan, former chairman of the Federal Reserve, former Treasury Secretary John Snow and Securities and Exchange Commission Chairman Christopher Cox testified before the U.S. House Committee on Oversight and Government Reform.

After testimony by the regulators, Committee Chairman Henry Waxman said "The list of mistakes is long and the cost to taxpayers is staggering......Our regulators became enablers rather than enforcers. Their trust in the wisdom of the markets was infinite. The mantra became that government regulation is wrong. The market is infallible."

After testimony by the regulators, Committee Chairman Henry Waxman said "The list of mistakes is long and the cost to taxpayers is staggering......Our regulators became enablers rather than enforcers. Their trust in the wisdom of the markets was infinite. The mantra became that government regulation is wrong. The market is infallible."

The Good News

According to the US Bureau of Economic Analysis, the personal savings rate is up! Big time, to about $297 billion at an annual rate for the second quarter 2008 (the latest data available)! http://www.bea.gov/national/nipaweb/Nipa-Frb.asp

The consumer should also be feeling the effects of the recent decrease in oil prices. Where I am at, this translates to about $3.00 per gallon, or a 25% decrease. This should help people a lot. However, will it be enough to offset increases in mortgage expenditures due to increased rates, etc.?

There is a negative for this saving at this time; it is not a good thing for the economy. It removes at an annual rate $297 billion. This essentially negates some of the government stimulus. However, longer term, this is a very, very good thing.

The consumer should also be feeling the effects of the recent decrease in oil prices. Where I am at, this translates to about $3.00 per gallon, or a 25% decrease. This should help people a lot. However, will it be enough to offset increases in mortgage expenditures due to increased rates, etc.?

There is a negative for this saving at this time; it is not a good thing for the economy. It removes at an annual rate $297 billion. This essentially negates some of the government stimulus. However, longer term, this is a very, very good thing.

Wednesday, October 22, 2008

Ask me in 20 Years!

I was asked recently if I am invested in the stock market. That question was prompted by our recent financial "crisis" and the current aftermath. The answer is YES! Here are my reasons:

- Both my spouse and I are employed. We do save a portion of our earnings each month and a substantial portion of these savings goes into retirement accounts.

- We are of an age where it is likely one of us will still be on this planet in 40 years. Look at it this way. Consider that today it is the year 1968 and that one of us will probably still be on the planet in the year 2008! From the perspective of 1968, that's a long, long way into the future. A lot can happen in 40 years, and probably will. For example, there were seven (7) bear or near bear markets in that period, including the "bear market of 2008-2009". So we need a financial plan which can accomodate that unknowable, somewhat distant future.

- Inflation is a long term concern.

- There is evidence that the stock market is a good hedge against inflation, over the long term.

- That portion of the funds we do have "invested" are in a diversified portfolio. That portfolio is somewhat conservative and includes dividend paying stocks, mutual funds and bonds.

- We are applying the principle of dividend reinvestment. Dividend yields are highest when the stock market is at the bottom, and dividend reinvestment ensures that new shares are purchased at these lower prices. In the super- or mega-bear market of 1773-74 and during the ensuing malaise when stock market indexes were flat for nearly 10 years, there were dividend yields of up to 5%. Those yields enabled substantially better total returns than the market indexes would suggest.

- We have some funds, including an "emergency fund" which are not invested in the stock market and we can tolerate waiting 10 years for a market return.

- We are doing our best to maintain a long term focus.

- We are aware there are risks. There is always the unknowable. It is possible neither of us will be alive in 5 years. It is also possible that we will both be alive in 40 years. So we do our best to plan for both possibilities.

So that is our rationale. On the other hand, it isn't easy watching the government hand over $$ of our taxes to the banks and investment bankers who contributed to this mess. Nor is it easy listening to the whining of those who want to help the "poor homeowners". Many of those "poor homeowners" were as greedy as the bankers who got us into this mess. I suppose some sort of intervention will be necessary. There are rational arguments both for and against. I suspect that the financial turmoil will not end until the housing market is stabilized. One good thing, "Wall Street" has finally gotten the "black eye" it has deserved! No matter who is elected as President in 2008, there will be some change in the way that Wall Street is treated in America.

I think it is important to seperate the housing problems from the economy at large. I don't know how people will adjust to the reality of the new credit landscape. The worst could be over in 6 months. However, I do think it will take years to sort some of this out, and that home prices will fall for perhaps 5 years or until 2013. That will not necessarily be universal, as "all real estate is local" as the saying goes. However, California in particular will have many single-family homes priced below their peak levels of 2006-2007. Home valuations in the hardest hit areas will probably be 50% of their peak value. This is not my SWAG here, I am presenting numbers I have distilled from many sources.

As the economy stabilizes and panic recedes, many people will realize that things aren't as bad as they thought they would be. The stock market will recover. In particular, there will be a need to invest and as housing will no longer be the rock star it once was, the stock market may be considered a reasonable place for such investments. I base this optimism on the recent past, most notably the aftermath of the internet boom and bust of 2002.

When I was asked "why am I invested in the stock market", the question could as easily have been "why am I invested in America?", for that is what I am doing. I have always had a faith in the ability of this amazing country to transcend certain problems and idiosyncrasies of human beings. However, the past 10 years have been trying, and have tested that faith. Should I be concerned? Yes, I think I should be! Should I panic? No, and to help me in that I will attempt to watch as little financial news as possible. (Note: keeping these blogs going and minimizing exposure is going to be a task; I'll definitely be avoiding most of the "popular" media and as many of the "talking heads" as possible).

One other thing I keep in mind. A lot of the financial news is generated in New York and as we know, that town is tightening it's belt and looking toward gloomier times. I am of the opinion that this will cloud the news emanating from that city. Consider it an internal bias to the news. I will be listening for that bias.

The bottom line: Have I made good decisions? How will it turn out? Ask me in 10 to 20 years!

PS: I know that the conventional wisdom is oil and other consumables will tank in a recession, or a serious recession. However, I couldn't pass up the opportunity to pick up some National Oilwell Varco (NOV)

Myths About the Financial Crisis of 2008

The Research Department of the Federal Reserve Bank of Minneapolis has published a paper with the title above:

http://www.minneapolisfed.org/research/WP/WP666.pdf

This is an 18 page document, consisting substantially of charts and diagrams. It states the following:

"The financial press and policymakers have made four claims about the nature of the crisis.

1. Bank Lending to nonfinancial corporations and individuals has declined sharply.

2. Interbank lending is essentially nonexistent.

3. Commercial paper issuance by nonfinancial corporations has declined sharply and rates have risen to unprecedented levels.

4. Banks play a large role in channeling funds from savers to borrowers.

Here we examine these claims using data from the Federal Reserve Board. At least based on data up until October 8, 2008, we argue that all four claims are false."

http://www.minneapolisfed.org/research/WP/WP666.pdf

This is an 18 page document, consisting substantially of charts and diagrams. It states the following:

"The financial press and policymakers have made four claims about the nature of the crisis.

1. Bank Lending to nonfinancial corporations and individuals has declined sharply.

2. Interbank lending is essentially nonexistent.

3. Commercial paper issuance by nonfinancial corporations has declined sharply and rates have risen to unprecedented levels.

4. Banks play a large role in channeling funds from savers to borrowers.

Here we examine these claims using data from the Federal Reserve Board. At least based on data up until October 8, 2008, we argue that all four claims are false."

The Non-Science of Campaign Economics

The New York Times had an article today entitled "On Health Plans, the Numbers Fly". The article began with "Economics, it is said, is the dismal science. Anyone paying close attention to the campaign debate over the economics of health care might wonder about the science part."

http://www.nytimes.com/2008/10/22/us/politics/22health.html?_r=1&pagewanted=print&oref=slogin

It is no sup rise to find that "economics as practiced in the political arena is often “just ideology marketed in the guise of science.”" to quote Dr. Uwe E. Reinhardt, a health economist at Princeton. To quote Dr. Reinhardt further, "It’s garbage in, garbage out....Every econometric study is an effort in persuasion. I have to persuade the other guy that my assumptions are responsible. Depending on what I feed into the model, I get totally different answers....I give a lecture on whether you can trust economists, and I tell them no,” Dr. Reinhardt said. “I tell them that if at the end of the year I tell you the time of day and you trust me, I have failed.”

It has been apparent for some time, that politicians work diligently to "cherry pick" the facts that support their position. Given their penchant for short term thinking, and the overwhelming desire to be elected, I am certain that they can and do say anything necessary to get the vote. Pandering in politics is an art form.

I have found it to be a lot of work to check the facts of the various candidates. That's probably why the vast majority of Americans prefer to go for the candidate that promises the most. It's the easiest and shortest route. Besides, one feels good in selecting a polished candidate. After voting for him or her, I can go back home and feel like I did my patriotic duty and saved the country, again! However, there is ample evidence that these people cannot deliver. They haven't delivered in my life time so what makes one so certain they can or will this time? Perhaps that is the incentive to register all of those 18 year olds out there. They haven't been listening to this for 40 years as I have, and they have the optimism of youth. Unfortunately, that's the same misguided, biologically based optimism which also drives many of them to practice unsafe sex, as well as take undue risks on the highway.

So when we listen to the McCain and Obama political camps spouting health care plans, alternative energy scenarios and budgets, I think it is wise to keep the advice of Dr. Reinhardt in mind.

http://www.nytimes.com/2008/10/22/us/politics/22health.html?_r=1&pagewanted=print&oref=slogin

It is no sup rise to find that "economics as practiced in the political arena is often “just ideology marketed in the guise of science.”" to quote Dr. Uwe E. Reinhardt, a health economist at Princeton. To quote Dr. Reinhardt further, "It’s garbage in, garbage out....Every econometric study is an effort in persuasion. I have to persuade the other guy that my assumptions are responsible. Depending on what I feed into the model, I get totally different answers....I give a lecture on whether you can trust economists, and I tell them no,” Dr. Reinhardt said. “I tell them that if at the end of the year I tell you the time of day and you trust me, I have failed.”

It has been apparent for some time, that politicians work diligently to "cherry pick" the facts that support their position. Given their penchant for short term thinking, and the overwhelming desire to be elected, I am certain that they can and do say anything necessary to get the vote. Pandering in politics is an art form.

I have found it to be a lot of work to check the facts of the various candidates. That's probably why the vast majority of Americans prefer to go for the candidate that promises the most. It's the easiest and shortest route. Besides, one feels good in selecting a polished candidate. After voting for him or her, I can go back home and feel like I did my patriotic duty and saved the country, again! However, there is ample evidence that these people cannot deliver. They haven't delivered in my life time so what makes one so certain they can or will this time? Perhaps that is the incentive to register all of those 18 year olds out there. They haven't been listening to this for 40 years as I have, and they have the optimism of youth. Unfortunately, that's the same misguided, biologically based optimism which also drives many of them to practice unsafe sex, as well as take undue risks on the highway.

So when we listen to the McCain and Obama political camps spouting health care plans, alternative energy scenarios and budgets, I think it is wise to keep the advice of Dr. Reinhardt in mind.

Tuesday, October 21, 2008

People Will Be Strange

We have experienced a significant financial shock, which resulted in a panic. To some, it looked like the end of the world, but it was not. However, this is not over yet, not by a long shot. That reality is just beginning to sink in. Most of us are in some form of denial, and will attempt to go back to "business as usual". The resistance to change is so ingrained in our lives! Within limits, denial will be useful, but there will be no "business as usual" and such a strategy will not work. We cannot avoid this.

Unfortunately, people have not yet adapted to the current reality. It is somewhat like a Jekyll and Hyde economy out there. We are in uncharted waters and we will be experiencing additional shocks, or after shocks. We are entering a nasty recession, not some mild blip on the radar and with it, a bear market with teeth. This will not be a short, shallow recession.

As a consequence, people will be a bit strange. Stress levels will be high. Many people will operate as if this is a mild recession, rather than the nasty thing it really is, and hope it will soon be over. It will get worse and we will experience lots of bad news in the months, and perhaps years, ahead. And, our stock portfolios will take a pounding. As we do this slow, inexorable downward spiral in fits and starts, anxiety will again rear it ugly head, not just once, but again and again, as the bad news continues coming. Cities and towns will succumb to the consequences of their poor financial planning. Some states may teeter on bankruptcy. The news will get worse, much worse, before it gets better. It's too bad we can't fast forward to mid 2009 or so, but that is the way it is and one might as well brace for the economic fits and starts.

In the midst of all of this, Americans will suffer withdrawal pains as the cheap credit with which we have funded our lives for these past years, is no longer available. How will we survive without our toys, without exercising that need for a quick fix and a spate of binge buying?

The good news? We are in the maelstrom and like a nasty storm that has been brewing on the horizon for some time, we are no longer observers but are in it, and we will be in the fight of it. The period of waiting with hushed breath is over. Most of us are resourceful and are capable of making good decisions and we will now have the opportunity to make them, and to use all of the stuff we have learned these many years while we sat, apprehensively waiting for this storm to arrive.

So relax, take a deep breath, and give your neighbors and co-workers a hand or at the very least, some slack. We are all in this together and at various times, it will be necessary for each of us to lend a hand to another, so we do get through this with decency and grace.

Unfortunately, people have not yet adapted to the current reality. It is somewhat like a Jekyll and Hyde economy out there. We are in uncharted waters and we will be experiencing additional shocks, or after shocks. We are entering a nasty recession, not some mild blip on the radar and with it, a bear market with teeth. This will not be a short, shallow recession.

As a consequence, people will be a bit strange. Stress levels will be high. Many people will operate as if this is a mild recession, rather than the nasty thing it really is, and hope it will soon be over. It will get worse and we will experience lots of bad news in the months, and perhaps years, ahead. And, our stock portfolios will take a pounding. As we do this slow, inexorable downward spiral in fits and starts, anxiety will again rear it ugly head, not just once, but again and again, as the bad news continues coming. Cities and towns will succumb to the consequences of their poor financial planning. Some states may teeter on bankruptcy. The news will get worse, much worse, before it gets better. It's too bad we can't fast forward to mid 2009 or so, but that is the way it is and one might as well brace for the economic fits and starts.

In the midst of all of this, Americans will suffer withdrawal pains as the cheap credit with which we have funded our lives for these past years, is no longer available. How will we survive without our toys, without exercising that need for a quick fix and a spate of binge buying?

The good news? We are in the maelstrom and like a nasty storm that has been brewing on the horizon for some time, we are no longer observers but are in it, and we will be in the fight of it. The period of waiting with hushed breath is over. Most of us are resourceful and are capable of making good decisions and we will now have the opportunity to make them, and to use all of the stuff we have learned these many years while we sat, apprehensively waiting for this storm to arrive.

So relax, take a deep breath, and give your neighbors and co-workers a hand or at the very least, some slack. We are all in this together and at various times, it will be necessary for each of us to lend a hand to another, so we do get through this with decency and grace.

How Bad the Recession? Waiting for the Other Shoe to drop!

Someone said it isn't rocket science to believe that the combination of the worst housing meltdown in 30 years, the worst financial crisis since the Great Depression, the bursting of the worst consumer debt bubble and the greatest government debt exposure in history, would result in a worse than usual economic recession.

Are we in a recession? Yes, it is official!

http://abclocal.go.com/ktrk/story?section=news/national_world&id=6460443

So what's next? Well, now there is talk about a severe "global" recession! Beyond that, your guess is as good as mine. However, the stock market is in what is considered to be an "oversold" condition and the value of some stocks is way, way below their norms. Some say this is a good time to go cherry picking.

We may get a nice rally at some point before the end of the year, as people recover from their initial shock and begin purchasing stocks again. But is the worst over? I doubt it, as in, we probably are not yet at the bottom of this bear market. It is typical in bear markets to experience a rally or rallies. These can result in an upswing of 10 to 20%, or more. However, the trend will remain downward until we reach the "market bottom". So we can expect a few more ups and downs and accompanying noise in the media.

If this recession is similar to the recessions of 1973-75 and 1981-82, unemployment will reach a peak of 10.8% and the recession will have a duration of 16 months. The current recession, if it lasts 16 months, would not end until the first quarter of 2010.

The Futurist has some data on past recessions which can be a guide: http://www.singularity2050.com/2008/10/a-history-of-stock-market-bottoms.html

However, some are predicting a long, drawn out decline that will continue until 2020! It is worth considering that substantial mortgage resets will continue into 2012. As for the duration of this recession, what's true? Well, this recession is the result of some "worst ever" events as I described above, so it would be reasonable to expect that it could very easily last longer or, be somewhat drawn out. It could be like the Japanese decline of 13 years (90%!) from 1990 to 2003, or it could be similar to the sideways U.S. market that lasted for 15 years from 1960 to 1975. It should be noted that the Japanese lowered their interest rates all the way to 0% during that country's prolonged recession, and it didn't help.

So here's an interesting chart that demonstrates the effect over several bear markets, and a scatter diagram:

http://dshort.com/charts/bear-markets.html?three-bears

http://dshort.com/charts/bear-markets.html?bear-scatter-chart

Additional note added 10/23/08:

What will it take to get this economy moving and the financial markets back to normal? Possibly time. According to the WSJ, which quoted Moody's, Economy.com: "About 7.3 million American homeowners are expected to default on their mortgages between 2008 and 2010, with 4.3 million of those losing their homes." That will take some time to sort out. Today Federal Deposit Insurance Corp. Chairman Sheila Bair "suggested the government give banks a financial incentive to turn troubled loans into more-affordable mortgages." In a prepared statement and testimony before the Senate Banking Committee, she cited the experience of the FDIC has had modifying the mortgages it acquired from failed thrift IndyMac Bancorp. Ms. Bair testified that the FDIC program is in its early stages, but that more than 3,500 borrowers have accepted the proposed modifications. There is a thorny problem in all of this. Consider the politics. The government purchases bad mortgages. Fine. But what happens when homeowners go delinquent on these government backed mortgages? Who is going to be the fall guy for ejecting thousand of home owners, those "little guys" and "families" out of their homes when they do default? And it is a sure thing that some of these people will default. The situation is that dire, and as the economy cools, unemployment will increase 3 to 5 percent. Some people will get burned.

Chairman Bair's testimony should be available on the FDIC website:

http://www.fdic.gov/news/news/speeches/chairman/spoct2308.html

Several comments:

Are we in a recession? Yes, it is official!

http://abclocal.go.com/ktrk/story?section=news/national_world&id=6460443

So what's next? Well, now there is talk about a severe "global" recession! Beyond that, your guess is as good as mine. However, the stock market is in what is considered to be an "oversold" condition and the value of some stocks is way, way below their norms. Some say this is a good time to go cherry picking.

We may get a nice rally at some point before the end of the year, as people recover from their initial shock and begin purchasing stocks again. But is the worst over? I doubt it, as in, we probably are not yet at the bottom of this bear market. It is typical in bear markets to experience a rally or rallies. These can result in an upswing of 10 to 20%, or more. However, the trend will remain downward until we reach the "market bottom". So we can expect a few more ups and downs and accompanying noise in the media.

If this recession is similar to the recessions of 1973-75 and 1981-82, unemployment will reach a peak of 10.8% and the recession will have a duration of 16 months. The current recession, if it lasts 16 months, would not end until the first quarter of 2010.

The Futurist has some data on past recessions which can be a guide: http://www.singularity2050.com/2008/10/a-history-of-stock-market-bottoms.html

However, some are predicting a long, drawn out decline that will continue until 2020! It is worth considering that substantial mortgage resets will continue into 2012. As for the duration of this recession, what's true? Well, this recession is the result of some "worst ever" events as I described above, so it would be reasonable to expect that it could very easily last longer or, be somewhat drawn out. It could be like the Japanese decline of 13 years (90%!) from 1990 to 2003, or it could be similar to the sideways U.S. market that lasted for 15 years from 1960 to 1975. It should be noted that the Japanese lowered their interest rates all the way to 0% during that country's prolonged recession, and it didn't help.

So here's an interesting chart that demonstrates the effect over several bear markets, and a scatter diagram:

http://dshort.com/charts/bear-markets.html?three-bears

http://dshort.com/charts/bear-markets.html?bear-scatter-chart

Additional note added 10/23/08:

What will it take to get this economy moving and the financial markets back to normal? Possibly time. According to the WSJ, which quoted Moody's, Economy.com: "About 7.3 million American homeowners are expected to default on their mortgages between 2008 and 2010, with 4.3 million of those losing their homes." That will take some time to sort out. Today Federal Deposit Insurance Corp. Chairman Sheila Bair "suggested the government give banks a financial incentive to turn troubled loans into more-affordable mortgages." In a prepared statement and testimony before the Senate Banking Committee, she cited the experience of the FDIC has had modifying the mortgages it acquired from failed thrift IndyMac Bancorp. Ms. Bair testified that the FDIC program is in its early stages, but that more than 3,500 borrowers have accepted the proposed modifications. There is a thorny problem in all of this. Consider the politics. The government purchases bad mortgages. Fine. But what happens when homeowners go delinquent on these government backed mortgages? Who is going to be the fall guy for ejecting thousand of home owners, those "little guys" and "families" out of their homes when they do default? And it is a sure thing that some of these people will default. The situation is that dire, and as the economy cools, unemployment will increase 3 to 5 percent. Some people will get burned.

Chairman Bair's testimony should be available on the FDIC website:

http://www.fdic.gov/news/news/speeches/chairman/spoct2308.html

Several comments:

- 3500 out of 7.3 million expected defaults is less than 0.05% of the mortgages which will default. We have a long, long way to go! I would be inclined to apply a margin of error to the foreclosure numbers in Chairman Bair's statement of +/-50% and that means that it is possible that 10 million homeowners could default!

- A default of 10 million would essentially reverse the housing gains made in the past 10 years. See: http://www.frbsf.org/publications/economics/letter/2006/el2006-30.html

What's a "Baby Boomer" to do?

Retirees and near retirees, including the "baby boomers" of which I am one, have been wondering how the financial meltdown will affect them. Here is the comment of one expert, as Quoted in the Wall Street Journal 10/21/08:

"Olivia Mitchell, a professor at the Wharton business school and a former member of a bipartisan commission established by President Bush to study possible reforms of the Social Security system, says the market crash should be a wake-up call for Boomers to "understand risk better," starting with the risk that they may live way past 64. "The Baby Boomers are going to have to work longer and eat less," Ms. Mitchell says. "And go back to what my mother was doing -- saving string.""

There you have it, from an expert!

The original article was entitled "Boomer Bust: How Will the Economy Rebound Without Post-War Babies Financing Their Harleys?"

http://online.wsj.com/article/SB122455140262652669.html

"Olivia Mitchell, a professor at the Wharton business school and a former member of a bipartisan commission established by President Bush to study possible reforms of the Social Security system, says the market crash should be a wake-up call for Boomers to "understand risk better," starting with the risk that they may live way past 64. "The Baby Boomers are going to have to work longer and eat less," Ms. Mitchell says. "And go back to what my mother was doing -- saving string.""

There you have it, from an expert!

The original article was entitled "Boomer Bust: How Will the Economy Rebound Without Post-War Babies Financing Their Harleys?"

http://online.wsj.com/article/SB122455140262652669.html

Monday, October 20, 2008

Was it Greed or Stupidity?

I saw an article on Henry Cisneros, Clinton's Top Housing Official. He now has some misgivings about the housing market:

http://www.nytimes.com/2008/10/19/business/19cisneros.html?_r=1&em&oref=slogin

I sent the article on to a friend with some comments. He replied with an email "Thanks for sending the article which I missed in my rush thru the day. I always thought he [Cisneros] was a bad guy, starting from the sex scandal and what I read about him....He is partly to blame. And there are zillions of others....In the housing disaster, more to blame nationally are the lenders who could have given fixed-rate mortgages but persuaded many people to take variable-rate loans which then turned sour, often containing verbal promises to turn the mortgages later into fixed-rate deals (which were lies)....For even educated people, understanding the terms of a mortgage are almost impossible. I am convinced that lobbyists for financial institutions made the contract language confusing....Next, consider Fannie May and Freddie Whatever. McCain blames them and Obama but consider the facts. While these two companies are huge, they are responsible only for 2% to 3% of the housing and mortgage disasters. And McCain's Rick Davis was chief lobbyist for Fannie Mae, receiving big bucks until one month ago.....But the real reason for the financial crisis is more with the packaged fiancial instruments that Wall Street sold around the world. Nobody--even the big guys--understands what the contents of these really are. My son....says even the sophisticated bankers do not. Blame the Congress (Republicans for 6 of the last 8 years), lobbyists and McCain for sticking to deregulation, and the phony "greed" mantra (as tough it is 100% Wall Street's fault now). The Dems are in for some of the blame but the root of all this goes back to Reagan and the start of deregulation....To quote McCain of two or three years ago, "Deregulation is good for the growth of our economy."

To this email I responsed as follows:

As they say, “The Road to Hell is Paved With Good Intentions”.

We are currently in the eye of the storm.

And yes, no one understands these collateralized debt obligations (CDOs) which were backed by asset and mortgage backed securities, because each contains pieces of thousands of mortgages, the true value and rating of which is unknown and would be difficult to determine.

The math was faulty; when constructing these financial instruments the failure or default rate for new non-collateral mortgages (0% down, no income, no asset “liar” mortgages) were assumed to be identical to “normal” or collateral (20% down) mortgages. This is of course ridiculous.

As I see it, the big failure was the ratings agencies. They gave these dubious instruments a rating identical to US Treasury bills and bonds. That is gross negligence. And yes, I do agree that they could not determine some of the underlying numbers. However, it is illogical to assume that a CDO or mortgage based security built from tranches (slices or pieces) of mortgages including sub-prime, sub-sub prime and so on, is as safe as a US Treasury bill and to rate them as such.

There have been a lot of articles alluding to this for the past several years. They were generally given titles such as “the disconnect of return to risk” and so on.

As has been said, there is more than enough blame to go around. Many politicians were eager to get the poor into their own homes; as is the case with many things, this is OK as long as the make-up is a very small percentage of the total mortgages. In the current “crisis”, the total number of houses sold included too many risky mortgages. As a consequence, we today have millions of people in homes they cannot afford to live in, or soon will not be able to afford to live in.

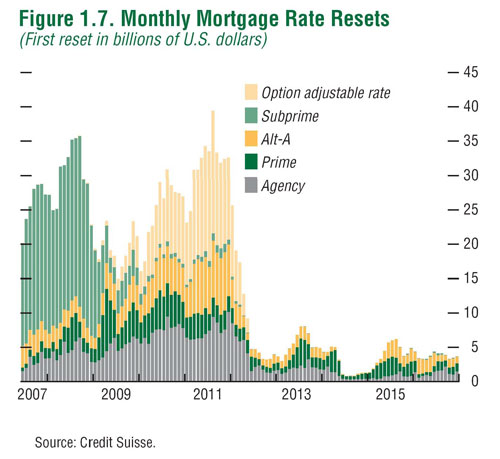

This is so because of the vast quantity of option-ARM loans out there. It is my understanding that these reset five years following the origination of the loan. However, these loans include a clause and if the borrower reaches a specific negative equity, somewhere in the range of 110% to 125% of the original loan balance, then the loan immediately resets to a higher rate. This some call a “surprise” reset. This event is automatic. It is anticipated that many option-ARM borrowers will face significantly higher monthly payment increases in the near future. How many? I saw a chart and it indicated loans totaling about $30 billion will reset in 2009 and as much at $70 billion will reset in 2010. These are not sub-prime loans.

As a result, defaults are expected to double again. Politicians or economists who expect the housing market crises will “bottom” in early 2009 are absolutely wrong, unless there is strong government intervention to prevent these automatic resets. This event is not a surprise. In March 2008, Goldman Sachs estimated that a 15% decline in housing values would occur and that 21% of the total number of people with a mortgage would owe more than their house was worth. However, it was also estimated that if a recession occurred then there would be a total decline in the value of housing of 30% and a whopping 39% of people owing mortgages would be under water. It is now a certainty that we are in or are entering a serious recession.

I am not certain if our government will intervene until it is too late. At present, congress is working on committees of lynching parties rather than averting this looming crisis. So batten down the hatches and be prepared for a potentially rough ride for the next two or three years.

Here is a chart to support what I said about loan resets:

http://www.goodevalue.com/wp-content/uploads/2008/04/imfresets.jpg

As for the “greed”, there are too many questions about that. Is it “greed” to expect to have things I cannot afford? Is it “greed” to expect to live in a house I cannot afford? Is it “greed” to want all of this stuff to the point that we feel entitled to our desires? When every man, woman and child in a nation expects that things will always turn out and that they can and will have in their lifetime whatever they want, at the expense of others, is that “greed”? Or simply stupidity?

http://www.nytimes.com/2008/10/19/business/19cisneros.html?_r=1&em&oref=slogin

I sent the article on to a friend with some comments. He replied with an email "Thanks for sending the article which I missed in my rush thru the day. I always thought he [Cisneros] was a bad guy, starting from the sex scandal and what I read about him....He is partly to blame. And there are zillions of others....In the housing disaster, more to blame nationally are the lenders who could have given fixed-rate mortgages but persuaded many people to take variable-rate loans which then turned sour, often containing verbal promises to turn the mortgages later into fixed-rate deals (which were lies)....For even educated people, understanding the terms of a mortgage are almost impossible. I am convinced that lobbyists for financial institutions made the contract language confusing....Next, consider Fannie May and Freddie Whatever. McCain blames them and Obama but consider the facts. While these two companies are huge, they are responsible only for 2% to 3% of the housing and mortgage disasters. And McCain's Rick Davis was chief lobbyist for Fannie Mae, receiving big bucks until one month ago.....But the real reason for the financial crisis is more with the packaged fiancial instruments that Wall Street sold around the world. Nobody--even the big guys--understands what the contents of these really are. My son....says even the sophisticated bankers do not. Blame the Congress (Republicans for 6 of the last 8 years), lobbyists and McCain for sticking to deregulation, and the phony "greed" mantra (as tough it is 100% Wall Street's fault now). The Dems are in for some of the blame but the root of all this goes back to Reagan and the start of deregulation....To quote McCain of two or three years ago, "Deregulation is good for the growth of our economy."

To this email I responsed as follows:

As they say, “The Road to Hell is Paved With Good Intentions”.

We are currently in the eye of the storm.

And yes, no one understands these collateralized debt obligations (CDOs) which were backed by asset and mortgage backed securities, because each contains pieces of thousands of mortgages, the true value and rating of which is unknown and would be difficult to determine.

The math was faulty; when constructing these financial instruments the failure or default rate for new non-collateral mortgages (0% down, no income, no asset “liar” mortgages) were assumed to be identical to “normal” or collateral (20% down) mortgages. This is of course ridiculous.

As I see it, the big failure was the ratings agencies. They gave these dubious instruments a rating identical to US Treasury bills and bonds. That is gross negligence. And yes, I do agree that they could not determine some of the underlying numbers. However, it is illogical to assume that a CDO or mortgage based security built from tranches (slices or pieces) of mortgages including sub-prime, sub-sub prime and so on, is as safe as a US Treasury bill and to rate them as such.

There have been a lot of articles alluding to this for the past several years. They were generally given titles such as “the disconnect of return to risk” and so on.

As has been said, there is more than enough blame to go around. Many politicians were eager to get the poor into their own homes; as is the case with many things, this is OK as long as the make-up is a very small percentage of the total mortgages. In the current “crisis”, the total number of houses sold included too many risky mortgages. As a consequence, we today have millions of people in homes they cannot afford to live in, or soon will not be able to afford to live in.

This is so because of the vast quantity of option-ARM loans out there. It is my understanding that these reset five years following the origination of the loan. However, these loans include a clause and if the borrower reaches a specific negative equity, somewhere in the range of 110% to 125% of the original loan balance, then the loan immediately resets to a higher rate. This some call a “surprise” reset. This event is automatic. It is anticipated that many option-ARM borrowers will face significantly higher monthly payment increases in the near future. How many? I saw a chart and it indicated loans totaling about $30 billion will reset in 2009 and as much at $70 billion will reset in 2010. These are not sub-prime loans.

As a result, defaults are expected to double again. Politicians or economists who expect the housing market crises will “bottom” in early 2009 are absolutely wrong, unless there is strong government intervention to prevent these automatic resets. This event is not a surprise. In March 2008, Goldman Sachs estimated that a 15% decline in housing values would occur and that 21% of the total number of people with a mortgage would owe more than their house was worth. However, it was also estimated that if a recession occurred then there would be a total decline in the value of housing of 30% and a whopping 39% of people owing mortgages would be under water. It is now a certainty that we are in or are entering a serious recession.

I am not certain if our government will intervene until it is too late. At present, congress is working on committees of lynching parties rather than averting this looming crisis. So batten down the hatches and be prepared for a potentially rough ride for the next two or three years.

Here is a chart to support what I said about loan resets:

http://www.goodevalue.com/wp-content/uploads/2008/04/imfresets.jpg

{kind=link}

As for the “greed”, there are too many questions about that. Is it “greed” to expect to have things I cannot afford? Is it “greed” to expect to live in a house I cannot afford? Is it “greed” to want all of this stuff to the point that we feel entitled to our desires? When every man, woman and child in a nation expects that things will always turn out and that they can and will have in their lifetime whatever they want, at the expense of others, is that “greed”? Or simply stupidity?

Things to Watch to Determine if the Economy is Improving

Short term, there are several indicators which can be observed to give an idea of the state of the economy:

1. The so called "TED spread" or difference between LIBOR and US Treasuries. Ideally, watch the 3 month figure, which is normally about 1%:

http://www.bloomberg.com/apps/cbuilder?ticker1=.TEDSP%3AIND

2. Commodities prices. Oil is a good indicator of confidence in the economy. Commodities and oil in free fall are an omen of lack of confidence. Consumption might also be useful to watch:

http://www.bloomberg.com/markets/commodities/cfutures.html

http://www.eia.doe.gov/emeu/international/crude2.html

http://www.bloomberg.com/apps/cbuilder?ticker1=DOEDMGAS%3AIND

3. Dollar weakening slightly against other currencies, most notably the Euro:

http://finance.yahoo.com/q/bc?s=USDEUR=X

Longer term, the inventory of existing homes for sale is a possible indicator:

http://www.data360.org/dsg.aspx?Data_Set_Group_Id=1395

http://www.realtor.org/research/research/ehsdata

Just for chuckles, here is a list of the prime rate. I was once one of the unlucky ones who had a home equity loan at the time the prime was 20%. My hat's off to former Fed Chairman Volcker! Ouch:

http://www.data360.org/dataset.aspx?Data_Set_Id=47

1. The so called "TED spread" or difference between LIBOR and US Treasuries. Ideally, watch the 3 month figure, which is normally about 1%:

http://www.bloomberg.com/apps/cbuilder?ticker1=.TEDSP%3AIND

2. Commodities prices. Oil is a good indicator of confidence in the economy. Commodities and oil in free fall are an omen of lack of confidence. Consumption might also be useful to watch:

http://www.bloomberg.com/markets/commodities/cfutures.html

http://www.eia.doe.gov/emeu/international/crude2.html

http://www.bloomberg.com/apps/cbuilder?ticker1=DOEDMGAS%3AIND

3. Dollar weakening slightly against other currencies, most notably the Euro:

http://finance.yahoo.com/q/bc?s=USDEUR=X

Longer term, the inventory of existing homes for sale is a possible indicator:

http://www.data360.org/dsg.aspx?Data_Set_Group_Id=1395

http://www.realtor.org/research/research/ehsdata

Just for chuckles, here is a list of the prime rate. I was once one of the unlucky ones who had a home equity loan at the time the prime was 20%. My hat's off to former Fed Chairman Volcker! Ouch:

http://www.data360.org/dataset.aspx?Data_Set_Id=47

Friday, October 17, 2008

The Chinese on China - The Milk Scandal

From the New York Times, today:

The background: "One of China’s largest milk companies, Sanlu, based in the city of Shijiazhuang, was the most prominent dairy producer found to sell milk products tainted with melamine, a toxic chemical illegally added to watered-down milk to artificially increase the protein count and fool safety tests."

"....the milk scandal involves a web of complicity linking company executives to government officials. Those connections make sorting out responsibility a delicate political task. Rather than allow the courts to weigh in, officials prefer to press complainants to take compensation, said Teng Biao, a lawyer in Beijing who is collecting material for a possible class-action lawsuit.

"Traditionally in China, politics is always higher than the law,” he said.

“To protect Sanlu is to protect the government itself,” he added. “A public health crisis like this not only involves Sanlu. It involves many officials from authorities in the city of Shijiazhuang up to the central government. It involves media censorship, the food quality regulatory system and the corrupt deal between commercial merchants and corrupt officials.”

Link to the article:

http://www.nytimes.com/2008/10/17/world/asia/17milk.html

The background: "One of China’s largest milk companies, Sanlu, based in the city of Shijiazhuang, was the most prominent dairy producer found to sell milk products tainted with melamine, a toxic chemical illegally added to watered-down milk to artificially increase the protein count and fool safety tests."

"....the milk scandal involves a web of complicity linking company executives to government officials. Those connections make sorting out responsibility a delicate political task. Rather than allow the courts to weigh in, officials prefer to press complainants to take compensation, said Teng Biao, a lawyer in Beijing who is collecting material for a possible class-action lawsuit.

"Traditionally in China, politics is always higher than the law,” he said.

“To protect Sanlu is to protect the government itself,” he added. “A public health crisis like this not only involves Sanlu. It involves many officials from authorities in the city of Shijiazhuang up to the central government. It involves media censorship, the food quality regulatory system and the corrupt deal between commercial merchants and corrupt officials.”

Link to the article:

http://www.nytimes.com/2008/10/17/world/asia/17milk.html

Thursday, October 16, 2008

Candidates Avoiding the Really Tough Issues

This from the Wharton School, University of Pennsylvania. Link to full article is below.

"In the closing weeks of the U.S. presidential campaign, the candidates are focused largely on the global financial meltdown, which is formidable enough. But looming behind this front-burner concern are the very difficult long-term economic challenges of restoring Social Security and Medicare to solid footing, and providing health care coverage to the millions of Americans who are uninsured or inadequately insured....."

"We were so concerned about the $700 billion in the bailout bill, but nobody is talking seriously about the $12 trillion we need to make Social Security whole and the $65 trillion we need to make Medicare whole," says Wharton professor of insurance and risk management Olivia Mitchell. She worries that that when it comes to Social Security and Medicare, both candidates are more focused on the revenue side of the equation than on addressing the rampant growth of benefit obligations which would require cuts for beneficiaries...."

"According to Wharton insurance and risk management professor Kent Smetters, a former Congressional Budget Office economist, the Obama proposal would place a high percentage of the tax burden on one, small segment of the population and would only generate about 20% to 30% of the revenue needed. "There's not much talk about how to control growth on spending -- that's the real issue," says Smetters. "If you get more revenue, it doesn't solve the problem until you can control spending....."

http://knowledge.wharton.upenn.edu/article.cfm?articleid=2070

"In the closing weeks of the U.S. presidential campaign, the candidates are focused largely on the global financial meltdown, which is formidable enough. But looming behind this front-burner concern are the very difficult long-term economic challenges of restoring Social Security and Medicare to solid footing, and providing health care coverage to the millions of Americans who are uninsured or inadequately insured....."

"We were so concerned about the $700 billion in the bailout bill, but nobody is talking seriously about the $12 trillion we need to make Social Security whole and the $65 trillion we need to make Medicare whole," says Wharton professor of insurance and risk management Olivia Mitchell. She worries that that when it comes to Social Security and Medicare, both candidates are more focused on the revenue side of the equation than on addressing the rampant growth of benefit obligations which would require cuts for beneficiaries...."

"According to Wharton insurance and risk management professor Kent Smetters, a former Congressional Budget Office economist, the Obama proposal would place a high percentage of the tax burden on one, small segment of the population and would only generate about 20% to 30% of the revenue needed. "There's not much talk about how to control growth on spending -- that's the real issue," says Smetters. "If you get more revenue, it doesn't solve the problem until you can control spending....."

http://knowledge.wharton.upenn.edu/article.cfm?articleid=2070

Tuesday, October 14, 2008

To quote Rod Serling, we are now in the Zone

"There is a fifth dimension beyond that which is known to man. It is a dimension as vast as space and as timeless as infinity. It is the middle ground between light and shadow, between science and superstition, and it lies between the pit of man's fears and the summit of his knowledge. This is the dimension of imagination. It is an area which we call the Twilight Zone."

The above is from the opening of the original Twilight Zone television program. It premiered October 1, 1959 on CBS.

The above is from the opening of the original Twilight Zone television program. It premiered October 1, 1959 on CBS.

Monday, October 13, 2008

Ouch!

What else can I say about the latest "bang" to our economy? The market dropped as panic selling took hold. I actually purchased some stock in the past week, looking toward the long term.

Is it gambling? Could be, as our political leaders are as clueless as ever. I watched Sen. Joe Biden at a political rally on C-SPAN and there was Sen. Hillary Clinton, head rhythmically moving up and down, looking so much like a bobble headed doll on his right.

This is getting close to my "worst case" scenario of about a 50% loss. The problem is, we haven't even "officially" entered the recession yet, and already the market was down 43% off it's high set about 1 year ago.

I do have to admit, I am glad the waiting is over. I have been waiting for this "bang" for a few years now. Perhaps it is me, but I really couldn't see how we could avoid this. Too many people way, way overextended, too many people making money by moving money around, too many people always willing to blame someone else, way too many people willing to live beyond their means, and too many people expecting it will all turn out well, no matter what they do.

I have always had confidence in the American system, but the past 10 years have put that confidence under quite a strain. I am of the opinion that we as a nation face quite a "headwind". Americans have been too willing to put their trust in politicians, who really do little but make laws about collecting and spending our money. There is no long term planning! Thanks to the Internet and 100s of cable TV channels, we all have access to the same "information" and the picture is not pretty.

I use the word "information" with some hesitation. There is actually little true information available on the popular media, which has evolved from that age when it bragged that "we don't report the news, we make the news" to the very modern "we are the news". So there's not much reason to watch TV or radio news. Even NPR and PBS are very narrow in their news focus, although there is some air time given to the BBC. While travelling across Nebraska last year, I was delighted to be within range of the Omaha PBS radio station and expected to be able to hear at least a part of General Petraeus testimony before congress. However, the NPR channel had decided to play religious music for the Jewish holy days, instead. So I did not hear that testimony until I returned home and was able to get a copy of the transcript.

Th current financial crisis will, I fear, accelerate the flight from the dollar and further erode our ability as a nation to accomplish the many daunting tasks which do face us. It will also make world cooperation far more difficult as people all over the world have realized that this emperor really doesn't have any clothes!

After reading this, you may wonder if I am optimistic or pessimistic. As a businessperson, I am optimistic. I think that American businesses can and will continue to innovate and to operate successfully within the strictures imposed by our politicians. As a citizen, I am pessimistic. We have no viable energy bill and, for example, the Democrat's proposal of $15B per year for 10 years is laughable and woefully inadequate. We still have 78 million baby-boomers who will be retiring in the near future and a broken social security ponzi scheme. We have a failed medical system in which all comers are rewarded if people are ill. Need I go on?

Is it gambling? Could be, as our political leaders are as clueless as ever. I watched Sen. Joe Biden at a political rally on C-SPAN and there was Sen. Hillary Clinton, head rhythmically moving up and down, looking so much like a bobble headed doll on his right.

This is getting close to my "worst case" scenario of about a 50% loss. The problem is, we haven't even "officially" entered the recession yet, and already the market was down 43% off it's high set about 1 year ago.

I do have to admit, I am glad the waiting is over. I have been waiting for this "bang" for a few years now. Perhaps it is me, but I really couldn't see how we could avoid this. Too many people way, way overextended, too many people making money by moving money around, too many people always willing to blame someone else, way too many people willing to live beyond their means, and too many people expecting it will all turn out well, no matter what they do.

I have always had confidence in the American system, but the past 10 years have put that confidence under quite a strain. I am of the opinion that we as a nation face quite a "headwind". Americans have been too willing to put their trust in politicians, who really do little but make laws about collecting and spending our money. There is no long term planning! Thanks to the Internet and 100s of cable TV channels, we all have access to the same "information" and the picture is not pretty.

I use the word "information" with some hesitation. There is actually little true information available on the popular media, which has evolved from that age when it bragged that "we don't report the news, we make the news" to the very modern "we are the news". So there's not much reason to watch TV or radio news. Even NPR and PBS are very narrow in their news focus, although there is some air time given to the BBC. While travelling across Nebraska last year, I was delighted to be within range of the Omaha PBS radio station and expected to be able to hear at least a part of General Petraeus testimony before congress. However, the NPR channel had decided to play religious music for the Jewish holy days, instead. So I did not hear that testimony until I returned home and was able to get a copy of the transcript.

Th current financial crisis will, I fear, accelerate the flight from the dollar and further erode our ability as a nation to accomplish the many daunting tasks which do face us. It will also make world cooperation far more difficult as people all over the world have realized that this emperor really doesn't have any clothes!

After reading this, you may wonder if I am optimistic or pessimistic. As a businessperson, I am optimistic. I think that American businesses can and will continue to innovate and to operate successfully within the strictures imposed by our politicians. As a citizen, I am pessimistic. We have no viable energy bill and, for example, the Democrat's proposal of $15B per year for 10 years is laughable and woefully inadequate. We still have 78 million baby-boomers who will be retiring in the near future and a broken social security ponzi scheme. We have a failed medical system in which all comers are rewarded if people are ill. Need I go on?

Friday, October 10, 2008

Paul O'Neil on "The Root Cause" of the Banking Crisis

Paul O'Neil as quoted in Business Week, October 13, 2008:

The root cause of this crisis was "A combination of things. It begins with the stupid idea that you can put people in homes who have no income, no wealth, no regular job history. [Then there's the notion ] that in this marvelous world we've created of complex financial instruments, the originator of the loan can throw [the mortgage] out into cyberspace and someone will put a guarantee on it and it'll be amalgamated with a bunch of other stuff. And even though there may be a 3% to 5% risk of default, that's a manageable risk, and nobody will bet hurt. It's all a fiction".

Note: Mr. O'Neil was deputy director of the Office of Management & Budget, then CEO of Alcoa, and finally Treasury Secretary.

The root cause of this crisis was "A combination of things. It begins with the stupid idea that you can put people in homes who have no income, no wealth, no regular job history. [Then there's the notion ] that in this marvelous world we've created of complex financial instruments, the originator of the loan can throw [the mortgage] out into cyberspace and someone will put a guarantee on it and it'll be amalgamated with a bunch of other stuff. And even though there may be a 3% to 5% risk of default, that's a manageable risk, and nobody will bet hurt. It's all a fiction".

Note: Mr. O'Neil was deputy director of the Office of Management & Budget, then CEO of Alcoa, and finally Treasury Secretary.

Wednesday, October 1, 2008

It is Time to Take Back Our Country from the Politicians

We need to transform this country. To do this we must move beyond the political status quo, and we need a 21st century transformational energy policy NOW!

I got a letter from Al Gore yesterday. OK, so it wasn’t really a letter prepared for me; it was a form letter sent to me because I am on the MoveOn.org mailing list. In many respects, it was similar to many emails and letters I have received during the past 10 years. This particular letter was written on behalf of a group called the DSCC.

The DSCC's purpose is a variation on the familiar theme of “take back America”. This time, they want me to send a donation to assist them in building a filibuster proof Senate with at least 60 Senators from the Democratic party.

I find it amazing that these people want me to join millions of Americans to take America and hand it to them on a gold platter! What they are essentially telling me is "Take back America from the Republicans and give it to us. We'll take care of it and of you."

I have been voting for about 40 years and I am absolutely convinced that none of these people is going to take care of me. Their promises keep getting greater and the debt keeps getting larger. Now it is over $10 Trillion and growing. After multiple Democratic and Republican governments we have no energy plan and we have no funds in the SS trust fund (only IOUs which our descendants will have to pay back). So much for the good life!

I have had enough!

The only way we will take back America is if WE THE PEOPLE take it for ourselves.If you have any doubts about who REALLY owns this country, then the events of the past few weeks should have been a “wake up call”. I am referring to the bill before the congress, HR3997 Emergency Economic Stabilization Act of 2008 and the senate version which some cynically call the “No Banker Left Behind” bailout.

If you have been watching the deliberations in the House and the Senate, you should have noticed a strange thing. While the politicians continually rail either for or against it, it is generally described as something that is vital and that “we must have”. But no one can actually say exactly why we must have this specific piece of legislation. I do understand the issues of credit markets seizing, etc. However, why do we need a bill with the specific tenants of this one, such as authorizing our government to use nearly $1 Trillion of taxpayer dollars to purchase distressed assets, including those of “foreign authorities and central banks” at prices which the government has already stated will be “above market value” and therefore just about guaranteed to lose money for the taxpayer? I know this is included in the legislation because I read HR3997, and Secretary Paulson has made testimony to the fact regarding the prices that will be paid. I suggest you go to this link and you will be given a summary of the first 32 pages of the bill and a link to download it:

http://foreverthecynic.blogspot.com/2008/09/full-text-of-hr-3997-emergency-economic.html

The bill gives the Secretary of the Treasury broad powers and has a mechanism to reward the same firms that got us into this mess. Such firms will be hired to manage the money, for a fee:

http://foreverthecynic.blogspot.com/2008/10/secretary-of-treasury-to-be-given-broad.html

Why on earth would we do these things? I don’t know, but everyone from Senator Obama to Senator McCain say it is absolutely vital that we do this, and do it NOW.

I’ll tell you what we really need; we need an energy policy that diverts the flow of the 100s of billions of dollars we send each year to oil rich countries and instead, returns it to our shores, where it can be used to rebuild the manufacturing and infrastructure of this country. But we won’t have the funds to do this unless we first develop our own sources of energy. Then each and every year, those $100s of billions that we don't send to despots and tyrants all over the world will be put to use here, in America. Once we have the power and electrical transmission systems on line, we can transition from oil based automobiles to electrics, which we have simultaneously developed with R&D funds provided to companies right here in the USA. We will have to expand and upgrade our electrical transmission system. We can then use any funds surpluses to alleviate the deficit and we can sell the technology we have developed to others all over the world.

We can become leaders in this 21st century endeavor. Washington is beginning to get the word; today for the first time I heard Senator Obama talk about improved electrical transmission system as part of infrastructure improvements, while defending the “bailout” bill before the Senate. However, Washington has a penchant for moving slowly on most issues.

This is not "new" news. But our politicians have ignored most of this for over 30 years. One must ask, why would they do that? Maybe this problem is simply too complex for them to understand, just like the financial system and markets of this country.

It is vitally important that each and every American get on board and press congress, the Senate and our President, whoever he may be, to make this a national priority of the greatest urgency. This is not something to do tomorrow. It is something that must occur today. This transcends party politics and many of the issues that our politicians use to maintain their status quo.

We can build a better future. Politicians have been talking about a “National Energy Policy” for over 30 years and have done absolutely nothing. NOTHING! There is only one way and that is for us, the citizenry to take back our government from the politicians. We are the owners. We are the taxpayers. It is our country, not theirs. They are but civil servants elected to do our bidding. It is time we began treating them as such and acting like the owners we are. TAKE BACK AMERICA FROM WASHINGTON – NOW!

It is our choice and it is our opportunity. We can continue to support politicians and their failed or non-existent policies or begin looking beyond the hollow issues our politicians use to maintain their status quo. We can live in the past, or we can choose our future. These are exciting times we live in, and to use that often quoted phrase “a crisis is a dangerous opportunity”. Let us not waste it. This election, there is only one platform to vote for and that is for the candidates who have made energy transformation of this country THE priority.

What do YOU think and what are YOU going to do about this?

I got a letter from Al Gore yesterday. OK, so it wasn’t really a letter prepared for me; it was a form letter sent to me because I am on the MoveOn.org mailing list. In many respects, it was similar to many emails and letters I have received during the past 10 years. This particular letter was written on behalf of a group called the DSCC.

The DSCC's purpose is a variation on the familiar theme of “take back America”. This time, they want me to send a donation to assist them in building a filibuster proof Senate with at least 60 Senators from the Democratic party.

I find it amazing that these people want me to join millions of Americans to take America and hand it to them on a gold platter! What they are essentially telling me is "Take back America from the Republicans and give it to us. We'll take care of it and of you."

I have been voting for about 40 years and I am absolutely convinced that none of these people is going to take care of me. Their promises keep getting greater and the debt keeps getting larger. Now it is over $10 Trillion and growing. After multiple Democratic and Republican governments we have no energy plan and we have no funds in the SS trust fund (only IOUs which our descendants will have to pay back). So much for the good life!

I have had enough!

The only way we will take back America is if WE THE PEOPLE take it for ourselves.If you have any doubts about who REALLY owns this country, then the events of the past few weeks should have been a “wake up call”. I am referring to the bill before the congress, HR3997 Emergency Economic Stabilization Act of 2008 and the senate version which some cynically call the “No Banker Left Behind” bailout.

If you have been watching the deliberations in the House and the Senate, you should have noticed a strange thing. While the politicians continually rail either for or against it, it is generally described as something that is vital and that “we must have”. But no one can actually say exactly why we must have this specific piece of legislation. I do understand the issues of credit markets seizing, etc. However, why do we need a bill with the specific tenants of this one, such as authorizing our government to use nearly $1 Trillion of taxpayer dollars to purchase distressed assets, including those of “foreign authorities and central banks” at prices which the government has already stated will be “above market value” and therefore just about guaranteed to lose money for the taxpayer? I know this is included in the legislation because I read HR3997, and Secretary Paulson has made testimony to the fact regarding the prices that will be paid. I suggest you go to this link and you will be given a summary of the first 32 pages of the bill and a link to download it:

http://foreverthecynic.blogspot.com/2008/09/full-text-of-hr-3997-emergency-economic.html

The bill gives the Secretary of the Treasury broad powers and has a mechanism to reward the same firms that got us into this mess. Such firms will be hired to manage the money, for a fee:

http://foreverthecynic.blogspot.com/2008/10/secretary-of-treasury-to-be-given-broad.html

Why on earth would we do these things? I don’t know, but everyone from Senator Obama to Senator McCain say it is absolutely vital that we do this, and do it NOW.